UK aid spending to 2029

Commissioner overview

In early 2025, the Independent Commission for Aid Impact (ICAI) published a short account of where and how UK aid was being spent. The intention was to provide a baseline against which future UK aid expenditure decisions could be compared, allowing ICAI to look again at patterns over the four-year Commission. In 2026, the UK government published three-year official development assistance (ODA) allocations and spending plans for the Foreign, Commonwealth and Development Office (FCDO), meaning we can do some of that analysis now. There are clear caveats: we are analysing allocations not actual spending; some detail is still outstanding; plans can change and comparisons with past expenditure data can be harder to make. These allocations do, however, give us a good idea of the government’s priorities and choices.

In total, the picture portrayed by these allocations represents possibly the most significant set of changes to UK development practice since the 2002 International Development Act. Three points are worth pulling out as clear positives in terms of evidence and alignment with global context:

- Returning to multi-year allocations and forward visibility is long overdue – volatility and lack of predictability since 2021 have without doubt damaged value for money.

- The level of global humanitarian need and the concentration of extreme poverty in fragile or conflict affected areas means that prioritising allocations to these countries makes sense.

- Using the multilateral system for scale and reach is a rational stance.

Other elements of the picture raise more questions or pose implementation challenges.

Across the new UK aid landscape, the starkest change is the almost total exit from bilateral programming in 11 of the UK’s longstanding development partners. Bilateral allocations in these countries reduce sharply to £5 million in the third year of the planning period. Most of these countries are in sub-Saharan Africa; many were at the forefront of past aid/development effectiveness approaches.

It can be argued, as the UK does, that partnerships should evolve and that now is the time to retire bilateral programming in these countries. However, debt servicing levels are rising, some countries are less able to absorb the shock of reduced aid financing, and four remain low-income. The UK intends these modest allocations of £5 million to enable partnerships based on access to UK expertise, complemented by investment from British International Investment (BII).

How will the UK deal with the following issues?

- Past experience shows that providing truly demand led expertise is not easy – will the UK be able to do this effectively through the new Communities of Expertise?

- BII and other development finance institutions have found it harder to invest at scale beyond middle-income and emerging markets – will BII’s new strategy deliver as hoped?

- Will the UK have the capacity to exit responsibly and rapidly from existing programmes, while also implementing a new approach?

- Will opportunities for development and poverty reduction be missed in low-income, more stable countries? How much central funding might be available to complement the original £5 million allocation?

As our analysis shows, all countries receiving allocations greater than £10 million from 2028-29 will be fragile, conflict-affected or have sizeable refugee populations. Of these, only Ethiopia and Nigeria were described as “priority development partnerships” in a March 2026 Ministerial statement. We understand from FCDO that Pakistan is also in this category. Most others were described as humanitarian or fragility-focused allocations. The UK has also now made its next international climate finance commitment. Analysis of those numbers suggests that climate financing will need to overlap significantly with the commitment to spending 70% of country allocations in fragile and conflict affected states. While climate vulnerability and conflict increasingly occur together, global trends show less adaptation or resilience spending in these countries. The UK has also made a commitment to increase the percentage of its bilateral programmes with a principal or significant marker for gender equality to 90%.

How will the UK deal with the following issues?

- Much bilateral spending will need to hit multiple objectives – addressing humanitarian need, advancing gender equality, and building climate resilience. Does past evidence suggest this is credible?

- Will there be meaningful attempts to integrate climate adaptation or resilience into programmes in fragile and conflict-affected states?

- Will a bilateral programme dominated by humanitarian need be able to balance immediate priorities with longer term objectives such as recovery, peacebuilding, and poverty reduction?

The hard business of government is the business of choice, and these allocations clearly represent choices – to use multilateral institutions as the main finance vehicle for poverty and climate-focused development, global health bodies for specific interventions, and a bilateral country programme focused very largely on humanitarian need. Alongside these are a continued expansion of BII investment with ambitious commitments to mobilisation, market level impacts and Least Developed Countries, and a significant rewiring of the UK’s expertise offer. Some questions remain, however, together with challenges of implementation, and there will be lots to monitor and reflect on over the next three years. For our part as ICAI, we will cover some of these issues in our coming work.

Liz Ditchburn

Commissioner

Key findings

The government has published three-year departmental official development assistance (ODA) allocations and Foreign, Commonwealth and Development Office (FCDO) spending plans for the first time since 2016-17. While providing an important increase in predictability, they signal a historic decline in UK aid of approximately £6.5 billion, or a 42% fall over the four years from 2023 to 2027-28.1 This financial year alone (2026-27) sees UK ODA fall by around £3.1 billion or 24%.2

While the reduction from the statutory ODA spending target of 0.7% to 0.3% of UK gross national income is officially a temporary one, there is no evidence of any planning for a return to 0.7% in the spending figures or accompanying government statements.

The spending plans reveal major shifts in the scale, nature and purpose of UK aid. “Traditional” bilateral development programming – typified by portfolios of country programmes providing support across a range of sectors – is being phased out. A group of 11 countries – including longstanding UK partner countries like Kenya, Tanzania, Rwanda and Malawi – will see their annual allocations progressively reduced to £5 million by 2028-29. This standard allocation appears to be FCDO’s estimate of the ODA budget required to facilitate “modernised” partnerships based on “British and international expertise” and investment through British International Investment (BII).

The focus of the UK’s country-specific aid will shift to countries experiencing humanitarian crises. The government has committed to providing 70% of its country allocations to fragile and conflict-affected countries, and has committed to spending approximately £1.4 billion in the places with the greatest humanitarian needs. While consistent with past levels of UK humanitarian aid, this will absorb a much larger share of a reduced aid budget. FCDO will continue large-scale humanitarian support in Ukraine, Sudan and Palestine, along with substantial allocations to other long-running humanitarian crises and to certain refugee-hosting countries.

This major change in direction will see many partner countries losing 80-90% of their current allocations. However, it results in limited overall change by region or country income level, proportionally speaking, as falling development aid is replaced with humanitarian support for low-income countries as a group.

The government has committed to providing around £6 billion in international climate finance (ICF) over a three-year period, representing a higher share of UK aid (21.2%) than in the past five years. Given limited space within the overall budget, UK ICF is likely to be concentrated in fragile settings.

Full figures on UK multilateral aid are not yet available, but are likely to be below historical levels at around 20% of UK ODA. The UK continues to be a major contributor to the concessional windows of the World Bank and the African Development Bank, which suggests that these institutions are now seen as the main channels for future development finance for low-income countries.

Capital contributions to BII continue at the slower pace of £143 million per year (1% of UK ODA). With new investments approaching £2 billion per year, BII will be an important part of UK development cooperation in many countries. However, while BII has enjoyed some success in diversifying its portfolio, it remains heavily concentrated in larger markets.

1. Introduction

In February 2025, the UK government announced a reduction of UK official development assistance (ODA) to 0.3% of gross national income (GNI) by 2027, in order to fund an increase in defence spending. After several years of volatility in the UK ODA budget, this is the largest fall yet – approximately a £6.5 billion or 42% drop over the four years from 2023 to 2027.

During the 2025 Spending Review, three-year ODA budgets (2026-27 to 2028-29) were allocated to departments3, and the Foreign, Commonwealth and Development Office (FCDO) has now published its own three-year ODA spending plans.4 This is the first time since 2016-17 that a three-year outlook on UK aid has been available.

The purpose of this report is to assess the allocative choices within those ODA spending plans. Using the 2025 ICAI report on ‘How UK aid is spent’ as a baseline, it identifies trends and patterns in the data. It is descriptive rather than evaluative, and analyses the data to draw out implications for the direction of UK development cooperation. It follows on from a May 2026 ICAI report on ‘The changing global context for development cooperation’.

The report illustrates some dramatic changes. Bilateral funding for development programming in many of the UK’s longstanding partner countries is being phased out in favour of knowledge-based assistance, multilateral support, and investment via the UK’s development finance institution, British International Investment (BII). UK bilateral aid will increasingly prioritise fragile and conflict-affected states, principally through humanitarian support.

Box 1: Methodology and limitations

The report is prepared primarily on the basis of public documents and data, together with some additional detail provided to ICAI by FCDO. Some figures quoted here – such as UK multilateral ODA – are incomplete, with further contributions still to be announced. Spending plans do not contain the detailed breakdowns available in the UK’s official statistics on past ODA spending, and are subject to change. While FCDO has published its three-year spending plans, other ODA-spending departments are yet to do so. The spending plans are provided by financial year – 1 April to 31 March – while aid statistics are based on the calendar year, which complicates comparison.

Despite these limitations, the available data enables us to draw some reasonable inferences about the future directions of UK aid. We have been as transparent as possible about our sources, assumptions and calculation methods.

2. Changing patterns in UK aid

UK aid continues its sharp contraction

The UK government has announced major changes in the scale, nature and distribution of UK ODA. UK aid is undergoing a historic reduction to 0.3% of GNI, falling from a peak of £15.3 billion in 2023 to a planned £8.8 billion in 2027-28 – a 42% decline.

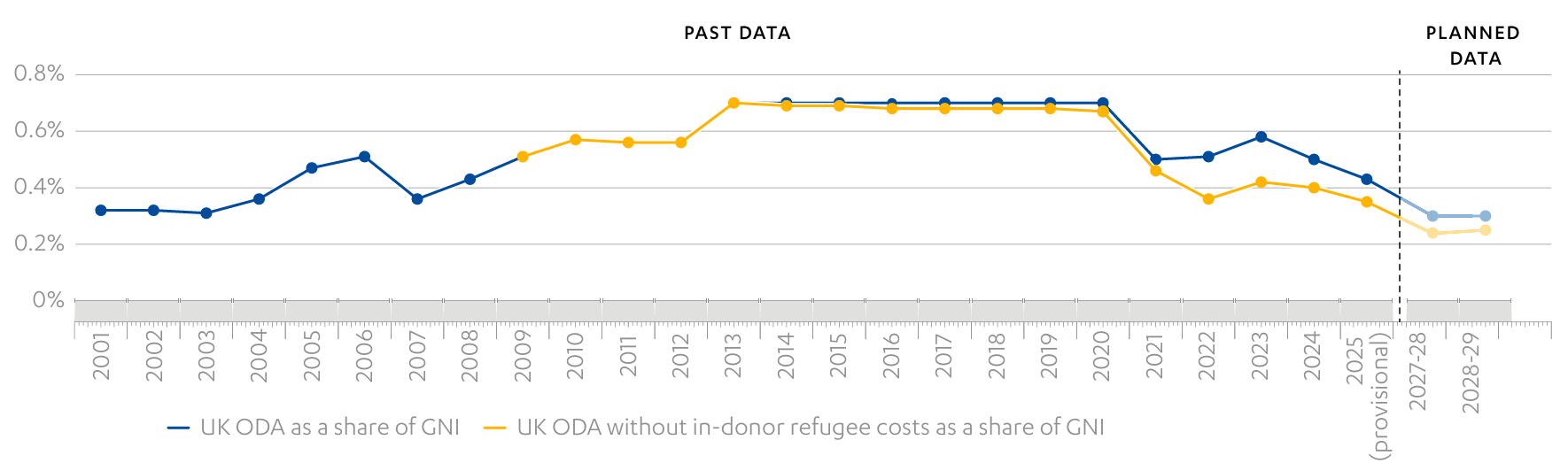

Figure 2 shows how UK aid has fallen from 0.7% to 0.3% of UK GNI over an eight-year period. If aid spent on support for refugees in the UK, known as in-donor refugee costs (IDRC)5 is factored out, the remaining ODA falls to a low of 0.237% of GNI in 2027-28 and then 0.25% in 2028-29. Non-IDRC ODA has only been that low once before (in 1999) in the 55-year history of UK aid.6

The government has restated its commitment to returning to the statutory ODA spending target of 0.7% of GNI when fiscal conditions allow.7 However, from Office for Budget Responsibility forecasts, this is not expected to occur before 2029, at the earliest. There is no evidence in the spending plans to suggest that the ongoing reductions in UK aid are seen as temporary.

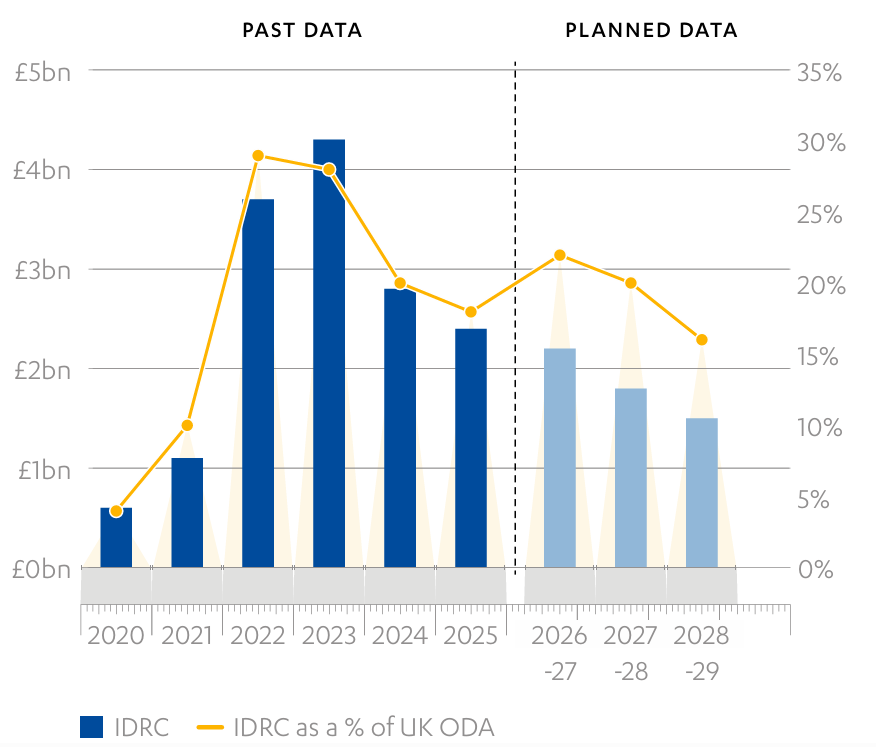

The spending plans continue to be influenced by high ODA spending on refugees in the UK. IDRC rose sharply in 2022 and 2023 to a peak of £4.2 billion (28% of all UK ODA), before gradually declining. Although not stated explicitly, departmental ODA allocations under the Spending Review appear to be based on the assumption that IDRC will be of the order of £2.2 billion, £1.8 billion and £1.5 billion in the three planning years8 (see Figure 1). This would represent 22%, 20% and 16% of total UK ODA over this period.

Figure 1: In-donor refugee costs (IDRC) are gradually coming down

Bar chart showing an upwards trend in IDRC from 2020 to 2023 before they start to decline from 2024 and in projections to 2028/2029.

Source: Foreign, Commonwealth and Development Office (FCDO) ‘Statistics on International Development’; HM Treasury, ‘Spending Review 2025’, June 2025; Independent Commission for Aid Impact, ‘Management of the official development assistance spending target 2021-25’, March 2026

Box 2: The end of FCDO’s ‘spender and saver of last resort’ role

In the past, the UK defined its annual ODA target as both a floor and ceiling, to be hit precisely each calendar year. It fell to FCDO to manage the target across departments, adjusting its own spending up or down in the last quarter of each year. Several ICAI reviews have analysed the negative impacts of this rigid approach to target setting.9

The role of ‘spender and saver of last resort’ has been removed from FCDO under the 2025 Spending Review. FCDO now has a predictable three-year allocation. However, while departmental allocations are based on an overall 0.3% ODA level, the government no longer guarantees that this will be achieved. If IDRC or UK GNI vary from predictions, UK ODA may end up above or below 0.3% of GNI.

Figure 2: UK aid as a share of gross national income (GNI) expected to reach historic low

Line graph showing total UK aid as a share of GNI trending upwards to reach 0.7% between 2013 and 2020, before falling to 0.5% and then to 0.3% in projections for 2028/29. When domestic refugee costs are removed from calculations, it follows the same trajectory but decreases further in all cases.

Source: Foreign, Commonwealth and Development Office (FCDO) ‘Statistics on International Development’; HM Treasury, ‘Spending Review 2025’, June 2025

Total UK ODA (without adjustment for inflation) fell sharply during 2020 and 2021, due to the impact of the pandemic on UK GNI and the decision to reduce the aid budget to 0.5%. It will fall even more sharply from 2023 to 2027, as the shift to a 0.3% budget is implemented, before rising in tandem with projected UK economic growth.

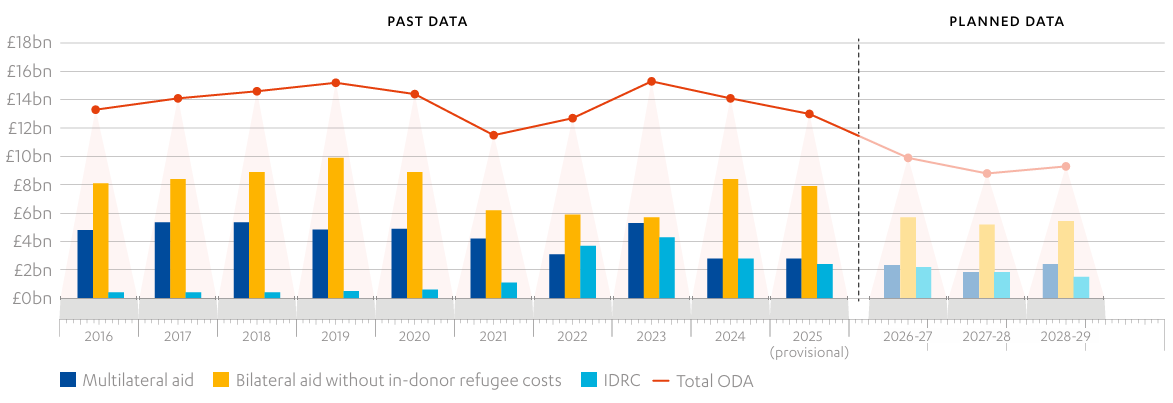

The first phase of reductions (July 2020) impacted most heavily on bilateral aid. Much of the UK’s multilateral aid is subject to multiannual agreements, making it harder to reduce in the short term. Multilateral aid also saw a sharp rise in 2023 – an artefact of FCDO varying the timing of payments across year end to manage the aid target in volatile conditions. Figures 3 and 4 show some of the larger trends in UK aid allocation. We do not yet have complete data on planned multilateral ODA for the next three years. The UK is yet to announce its contributions to the Global Environment Facility and the Global Partnership for Education, and other pledges may be made over the three-year planning period. Based on commitments to date, multilateral aid looks likely to be lower, as a share of UK aid, than it was in the period before 2020. FCDO has also pledged to increase the share of in-country programmes delivered by multilateral organisations (known as ‘multi-bi’ – see Box 3).

The decline in UK aid mirrors an unprecedented decline in global ODA flows. Global ODA fell by 23.1% in 2025 – the largest fall in history – with the five largest donors (Germany, the United States, the UK, Japan and France) all announcing reductions.10 The Organisation for Economic Co-operation and Development (OECD) projects further declines of 5.8% in 2026 and 10-18% in the following years, potentially taking global ODA back to levels last seen in the 2010-15 period.

Box 3: A typology of UK aid

Multilateral aid: Aid provided as core funding to multilateral organisations and available for onward allocation across countries.

Bilateral aid: All other UK aid, where the UK directly specifies the use of the aid.

Multi-bi aid: UK bilateral contributions to multilateral pooled funds or programmes and earmarked for specific uses.

In-donor refugee costs: Temporary support for refugees and asylum seekers during their first year in the UK, in accordance with international ODA reporting rules.

Figure 3: How UK aid is allocated across multilateral and bilateral spend

Bar chart showing multilateral aid, bilateral aid without in-donor refugee costs (IDRC) and IDRC for 2016 to 2025 and projected allocations to date. A line chart shows total ODA over the same periods. Both bar and line charts show that from a peak in 2023, UK ODA spending has fallen steadily and is planned to fall until 2027-28, before a slight increase in 2028-29. The bar chart shows that since 2022, IDRC costs have risen sharply, and though decreasing over time, are planned to occupy a similar share of ODA as multilateral spending, until 2028-29.

Source: Foreign, Commonwealth and Development Office (FCDO) ‘Statistics on International Development’ 2025; HM Treasury, ‘Spring Forecast 2026 speech’, 3 March, 2026; Independent Commission for Aid Impact, ‘Management of the official development assistance spending target 2021-25’, March 2026; Other data provided by FCDO

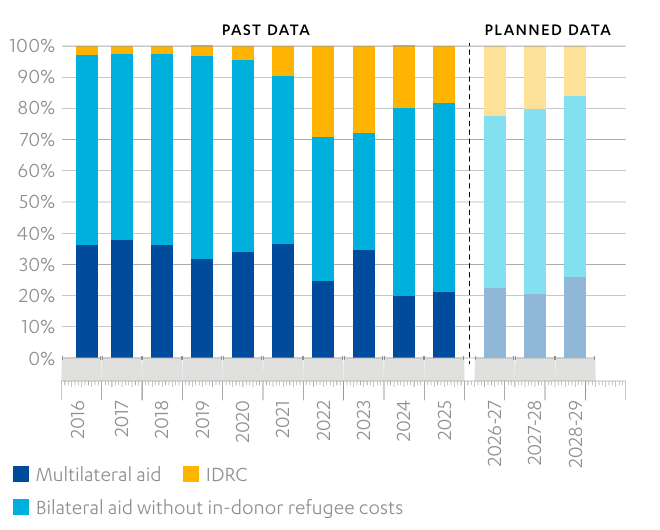

Figure 4: The multilateral share of UK aid has declined

Bar chart showing multilateral and bilateral aid as a share of non in-donor refugee (IDRC) costs and ODA, with projected allocations announced to date.

Source: Foreign, Commonwealth and Development Office (FCDO) ‘Statistics on International Development’ 2025; Independent Commission for Aid Impact, ‘Management of the official development assistance spending target 2021-25’, March 2026; other data provided by FCDO

UK bilateral aid is shifting away from traditional development programmes

The UK has announced a shift away from bilateral programming towards “modernised” development partnerships that combine reduced ODA with expertise, and investment through British International Investment (BII).

“The UK is modernising international development – delivering greater impact, value for money, and transparency. We’re shifting from donor to investor, sharing UK expertise to help countries thrive. Partnership, not paternalism is our new approach.”

Baroness Chapman, X, 22 July 2025

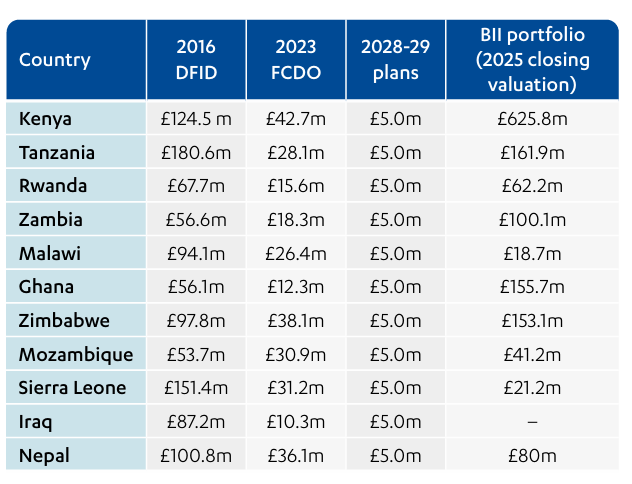

This shift is visible in FCDO’s planned country allocations. As Table 1 shows, a group of 11 countries will see their allocations fall each year, down to £5 million in 2028 29. Rather than funding “traditional” development programmes, this standard allocation will be used to facilitate partnerships based on knowledge sharing and investment. The phasing out of current development programmes looks likely to be rapid. Many of these countries face 50% reductions in each of 2026-27 and 2027-28, followed by a final step down to £5 million in 2028-29 – a decline of 80-90% over three years.

The countries in this group are longstanding partners for UK development cooperation (Table 1 shows their allocations of UK aid in 2016 and 2023). They are diverse in terms of income levels, ranging from Colombia ($7,919) to Malawi ($522) in per capita gross domestic product (GDP),11 suggesting that poverty levels are not the primary consideration behind the allocation. Some have graduated from low-income country (LIC) to lower-middle-income country (LMIC) status since 2016, which in principle makes them less dependent on ODA as a source of development finance. However, as discussed in ‘The changing global context for development cooperation’, as a group they face high debt pressure and limited access to affordable finance.

Rwanda, Malawi, Mozambique and Sierra Leone remain LICs. Malawi, for example, is one of the poorest countries in the world, with 75% of the population living on less than $3 per day and 51% below minimum calorie intake. Increasing exposure to climate shocks – including drought and storms – is leading to rising food insecurity12. In the recent past, the UK has run programmes in Malawi on education, health, family planning, nutrition, and water and sanitation, as well as providing periodic humanitarian support. The OECD projects that low-income and sub-Saharan countries like Malawi are the worst affected by bilateral ODA reductions, standing to lose a key source of funding for poverty-focused programming.13

The UK has also announced that it will no longer provide traditional bilateral funding for G20 countries.14 Consequently, aid allocations for Indonesia and South Africa will fall to zero by 2028-29. Turkey remains the exception, where the UK will continue to support Syrian refugees with a view to reducing onward migration to Europe.15

As Table 1 shows, BII has substantial investment portfolios in some of these countries, where it is set to become the primary conduit for UK ODA. However, in other countries BII struggles to find investment opportunities at scale.

Table 1: A number of traditional development partners will receive £5m allocations from 2028-29

In addition to these country allocations, partner countries may have access to technical assistance via a number of ‘Communities of Expertise’, which FCDO describes as “dynamic, demand-led, interdisciplinary hubs that bring together the best of UK and global expertise to help address mutual challenges in areas where partners most want to work with the UK”.16

Bilateral aid is now focused primarily on fragile and crisis-affected countries

The primary focus of UK bilateral aid is shifting to humanitarian assistance and to fragile and conflict-affected countries. UK humanitarian aid fell sharply in the 2021-23 period, but was then restored in 2024 to pre-pandemic levels. Over the next three years, the government plans to spend approximately £1.4 billion per year in places with the greatest humanitarian need, which represents around 15% of UK bilateral aid (consistent with the pre-pandemic period), and 78% of all FCDO aid allocated to specific countries and regions. The UK has also committed to spending 70% of its country allocations in fragile and conflict-affected states by 2028, which is reflected in the figures.

The spending plans show this new focus very clearly. All countries with allocations above £10 million in 2028-29 (see Table 2) either have live UN humanitarian appeals or substantial refugee populations. The spending plans do not indicate how much of the allocation is humanitarian, but the total for this group of countries in humanitarian need comes to approximately £1.4 billion, which aligns with the government’s planned spend in places with the greatest humanitarian need.

Within this list of fragile contexts, there are three distinct groups. The UK has identified Ukraine, Sudan and Palestine as top priorities. These are protected from any reductions. The UK’s ‘100-year partnership’ with Ukraine17 includes a wide range of support, including governance reforms, reconstruction, humanitarian assistance and fiscal support via guarantees.

A set of protracted humanitarian situations (Afghanistan, DR Congo, Myanmar, Somalia, South Sudan, Yemen) receive 25-30% reductions in 2026-27, and flat allocations after that. Finally, a group of countries that historically had a mixture of development and humanitarian programming (Bangladesh, Ethiopia, Pakistan, Nigeria) receive approximately 50% reductions in 2026-27 and flat allocations thereafter. FCDO documents suggest that they will continue to receive mixed development and humanitarian funding.

Ethiopia is a large country with complex development challenges – human development indicators in rural areas are alarmingly low, and a succession of shocks and crises in recent years has led to rising poverty and food insecurity.18 The UK has in the past provided large-scale support for education, maternal and child health, water and sanitation, agricultural development and nutrition, among other sectors. Ethiopia has also experienced large-scale civil conflict in recent years, and in 2024 received around £80 million in UK humanitarian support.19 UK bilateral support for Ethiopia will be reduced to £80 million by 2028-29.

Table 2: All countries with allocations above £10m face conflict, humanitarian crises or high refugee numbers

Note: A list of fragile and conflict-affected situations (FCAS) is released annually by the World Bank Group (WBG)

FCDO allocations by region and country income category mirror patterns of conflict and humanitarian need

FCDO’s total budget for country and regional programming will be £1.8 billion by 2028-29 – only slightly lower than the 2023-24 baseline.

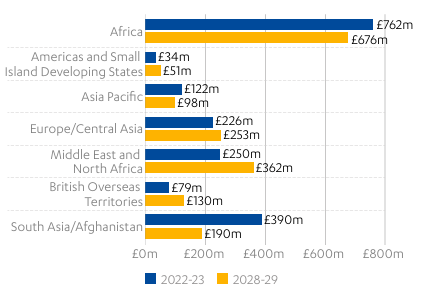

The increased focus on fragile and crisis contexts leads to some regional shifts. Africa, Asia-Pacific and South Asia all see declining allocations – proportionally and in monetary terms – while the Middle East and North Africa (MENA) and Europe/Central Asia see increases. This is consistent with large humanitarian responses in Palestine and other Middle Eastern conflict settings, and with the ringfencing of the Ukraine allocation.

Box 4: The UK continues to support ODA-eligible Overseas Territories (OTs)

The OT allocation rises from £88.7 million in 2023 to £130 million for each of the three planning years. It covers Montserrat, St Helena, Tristan da Cunha and the Pitcairn Islands. These territories are largely self-governing, but have a call on the aid budget for assistance where they are not financially self-sufficient. The rising allocation reflects the relatively high costs of maintaining essential infrastructure and services on remote islands with small populations, and their growing exposure to climate risks.

Figure 5: UK aid plans show limited change in regional allocations

Bar chart showing that regional allocations for UK aid have remained broadly similar between 2022-23 and 2028-29. There are modest projected increases for the Middle East and North Africa, Europe/Central Asia, and the British Overseas Territories, and a significant drop for South Asia/Afghanistan.

Source: Foreign, Commonwealth and Development Office. ‘Annual Report and Accounts 2024-2025’, July 2025, page 267; Other data provided by FCDO

FCDO’s overall country allocation shows no significant change by country income group. Looking solely at FCDO country allocations over £5 million (excluding OTs), we compared the 2028-29 allocation by country income group against the 2023 baseline. We found little change, proportionally speaking. LICs will receive 52%, which suggests that declining allocations for development programming in LICs will largely be replaced by humanitarian spending. LMICs will receive 45%, while the 2.3% to upper-middle-income countries is dominated by Turkey, with smaller allocations for Iraq and Colombia.

The UK retains a strong commitment to international climate finance

The UK has made a renewed international climate finance (ICF) commitment of around £6 billion for the three-year planning period. When compared to £11.6 billion for the previous five years, the new ICF commitment is a slightly lower rate of expenditure but a larger share, on average, of total ODA.

However, ICAI reviews have raised concerns that the previous target was achieved in part by changing the accounting methods for ICF, thereby “moving the goalposts”.20 The definition of ICF used in the next spending period will therefore be important.

The new pledge is accompanied by a commitment to provide an additional £6.7 billion in non-ODA climate finance, which includes lending from multilateral development banks mobilised through UK guarantees and export guarantees provided through UK Export Finance. BII’s 2026-31 strategy also includes a commitment to provide between £2.8 and £3.2 billion in climate investment over the five years, and a target to mobilise an additional £3.5 billion through its British Climate Partners initiative.

UK ICF will continue to be managed by several departments, including the Department for Energy Security and Net Zero (DESNZ), the Department for Environment, Food and Rural Affairs (Defra) and the Department for Science, Innovation and Technology (DSIT). FCDO will spend the largest share, with at least £4.6 billion over the three-year period. ICF is a cross-cutting label, rather than a separate budget, and therefore overlaps with development and humanitarian support. The available figures suggest that FCDO’s ICF spending will need to coincide substantially with its commitment to spend 70% of its country allocations in fragile and conflict-affected states.

The UK has reduced its planned contribution to the Green Climate Fund (GCF) for the 2024-27 period by half, to £815 million, of which £655 million has already been paid. Given the UK’s status as a leading contributor to the GCF, commentators have raised concerns that this decision may encourage other countries to follow suit.21

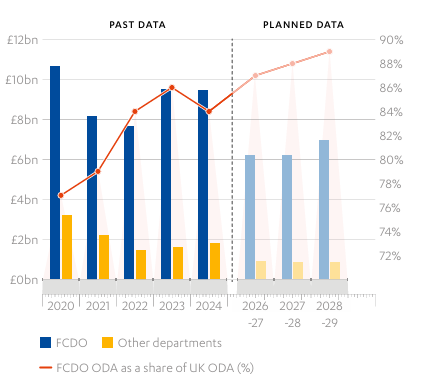

FCDO will spend a higher share of UK ODA

Over the decade to 2020, the ODA budget was increasingly shared across UK departments. The rise of IDRC, which is spent by the Home Office and a range of other departments, has exacerbated this trend. Over the coming three years, FCDO will spend between two-thirds and three-quarters of UK ODA. However, if IDRC is excluded (as shown in Figure 6), there is a consolidation back to FCDO, which will spend 89% of other ODA in 2028-29.

Figure 6: The Foreign, Commonwealth and Development Office (FCDO) share of overseas aid spending is gradually increasing

Bar chart comparing FCDO’s ODA (excluding in-donor refugee costs) with that of other departments, and as a percentage share of UK ODA. While ODA falls overall, FCDO is projected to spend over 87% of it from 2026-27.

Source: Foreign, Commonwealth and Development Office (FCDO) ‘Statistics on International Development’; HM Treasury, ‘Spending Review 2025’, June 2025

The UK continues its strong support for the multilateral development banks

Just over £3 billion in contributions over the three planning years will go to the multilateral development banks (MDBs), which the UK sees as the primary source of concessional (low-interest) development finance. The UK has made three-year pledges to the concessional windows of three MDBs – shown in Table 3 (alongside the previous two pledges, for comparison).

Table 3: UK multilateral development bank pledges by replenishment round

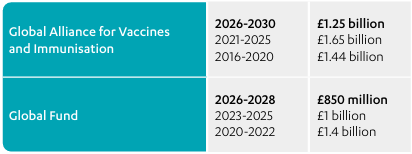

Global health bodies will receive £1.9 billion in UK contributions, concentrated in the Global Alliance for Vaccines and Immunisation (Gavi) and the Global Fund, which tackles AIDS, malaria and tuberculosis.

Table 4: UK pledges to global health bodies

International humanitarian bodies will receive £555 million and other UN agencies £170 million. A declining amount (£393 million) of UK aid is still channelled through European Union institutions, as part of a deal that the UK would continue funding long-running development projects (such as major infrastructure) approved before Brexit until their completion.

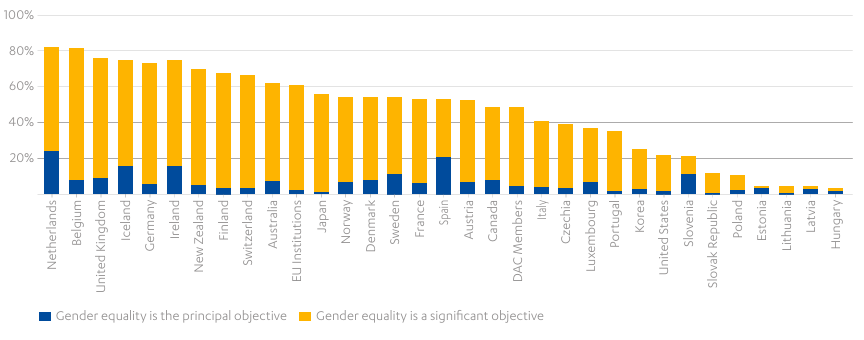

The UK has increased its target for gender equality programming

FCDO has set itself a target that at least 90% of its bilateral ODA programmes will have a focus on gender equality by 2030. The target refers to the OECD Gender Equality Policy Marker. In international aid statistics, this allows ODA to be tagged as:

- Principal: Gender equality is its primary objective.

- Significant: Gender equality is an important and deliberate objective, but not the main rationale.

- Not targeted: Neither principal nor significant

FCDO’s commitment is that 90% of all its programmes will be tagged as ‘principal’ or ‘significant’. The department claims that it achieved 81% in 2024, up from 58% in 2022, and is therefore on track for the 2030 target.

Figure 7 shows that, in 2023-24, the UK’s 75.6% put it third in the donor rankings for the OECD gender marker system. No country has ever achieved 90%.

Other donor countries have a higher share of their aid going to programmes rated as ‘principal’. However, a March 2026 equality impact assessment of FCDO programme allocations over the planning period noted that additional funds had been allocated to FCDO’s Human Development Directorate, to protect central spending on preventing violence against women and girls, preventing sexual violence in conflict, and women, peace and security.22

There are a number of challenges with ensuring that this target results in a meaningful shift in gender equality programming, particularly in mainstreaming practice. The marker system relies on self-reporting by programme managers, and concerns have been raised about the quality of the data in international aid statistics.

FCDO informs us that it has a quality assurance process, which involves word-searching business cases and flagging discrepancies. It also provides training and awareness raising to staff on gender equality, and targeted technical support to teams with a lower proportion of gender targeted programming.

However, screening is done at approval stage, based on business cases. ICAI has noted in past reviews that programme activities often evolve considerably during launch and implementation, with the risk that gender focused activities may be deprioritised.

Figure 7: The UK ranked third globally under the OECD gender marker system in 2023-24

Bar chart showing percentage of programmes labelled as having gender equality as a principal or significant objective across countries. The UK’s figure is around 75%, behind the Netherlands and Belgium.

Source: Organisation for Economic Co-operation and Development. ‘Development Finance for Gender Equality dashboard’ (viewed 17 June 2026)

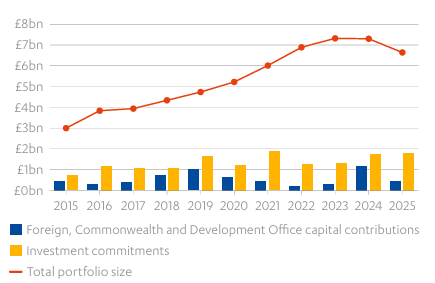

British International Investment will be an important part of UK development cooperation

The UK government is moving “from donor to investor” – one of four shifts in its changed approach to development cooperation. UK development investment is delivered mainly through British International Investment (BII, formerly CDC Group), which has grown rapidly over the past decade, becoming one of the world’s largest bilateral development finance institutions.

Between 2015 and 2025, BII received nearly £6 billion in capital contributions, averaging around 4% of UK ODA. In the coming three years, it will receive smaller contributions of £143 million each year, or 1% of UK ODA. However, as Figure 8 shows, BII’s portfolio reached £6.6 billion in 2025, and now generates more than £1 billion in cash to reinvest each year, even without new FCDO contributions.

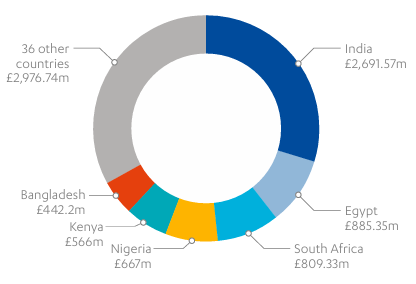

As Figure 9 shows, the BII portfolio remains concentrated in large middle-income countries, where there are more investment opportunities. Under its 2026 strategy, BII has pledged that at least 25% of new core investments will go to UN-designated Least Developed Countries, especially in Africa.23 The new strategy also states that BII expects to mobilise an additional £6-7.5 billion in private capital through its investments. Just under half of this is expected to be in the climate field, where investment opportunities in areas such as clean energy transition are relatively abundant. As we noted in ‘The changing global context for development cooperation’, development finance institutions have enjoyed mixed success so far in mobilising new investment on any scale in low-income settings.

Figure 8: The British International Investment (BII) portfolio has grown rapidly

Bar and line graph showing BII capital contributions, commitments and net assets from 2015 to 2025, when BII’s portfolio reached £6.6 billion.

Source: British International Investment. ‘Annual Accounts 2024’; Foreign, Commonwealth and Development Office. ‘British International Investment (BII) Programme of Support in Africa, South Asia, Indo Pacific & Carib (2015-2027)’

Figure 9: The portfolio remains heavily concentrated in larger markets

Pie chart showing top six British International Investment (BII) investee countries by net assets. India has the highest value of net assets while Kenya, Egypt, South Africa, Bangladesh and Nigeria make up the others.

Source: British International Investment. ‘Annual Reports’ (viewed 11 June 2026)

3. Conclusion

A major shift in the strategic direction of UK aid

The UK aid budget has been through a long period of disruption since the declaration of the global pandemic in 2020. The rapid rise of domestic refugee costs, and government decisions to reduce the UK aid budget from the statutory level of 0.7% of GNI, first to 0.5% in 2021 (in response to the fiscal pressures caused by the pandemic) and then to 0.3% from 2027 (to fund an increase in defence spending), have made advance planning very difficult.

The publication of three-year departmental ODA allocations and FCDO spending plans is therefore an important return to predictability. Earlier ICAI reviews have found that continuous budgetary uncertainty has been as disruptive as budget reductions.24

The reduction to a 0.3% aid budget is officially a temporary measure, until fiscal conditions permit a return to the statutory target. However, this return is not expected to occur before 2029 at the earliest, and nothing in the current spending figures or related government statements suggests any preparations for an eventual return to 0.7%. We note that the UK is one of several major donors currently scaling back its ODA spending, putting in doubt whether the global consensus around the UN’s 0.7% voluntary ODA commitment remains in place.

The spending figures illustrate dramatic changes in the nature and purpose of UK aid. They show that in-country, grant-based development finance for poverty reduction is coming to an end. Many of the UK’s longest-standing development partnerships are being reduced progressively to standard £5 million annual allocations – reductions of 80% or more from the 2023 baseline. These allocations are primarily intended to facilitate new partnerships based on UK expertise and investment, and it is not clear what proportion, if any, will fund “traditional” development programming.

Among the group of 11 countries that will receive £5 million allocations from 2028-29, some have graduated to lower middle-income country status, meaning that they are less dependent on ODA. As discussed in ‘The changing global context for development cooperation’, these countries nonetheless face rising debt pressure and limited access to affordable development finance. The group also includes low-income countries, such as Malawi and Sierra Leone, that remain heavily aid-dependent and may be hard-pressed to sustain national development expenditure as global ODA flows decline.

UK bilateral aid is being replaced by “UK and international expertise” and development finance investment through British International Investment (BII), as well as continuing concessional support from the multilateral development banks. However, BII is yet to identify investment opportunities at any scale in many of these countries.

Fragile and conflict-affected states are now the major focus of UK bilateral aid. The intent to spend approximately £1.4 billion per year in places with the greatest humanitarian need represents 78% of all FCDO aid allocated to specific countries and regions. All countries receiving more than £10 million allocations from 2028-29 will be crisis-affected or have significant refugee populations.

While this is a major shift at the country level, it does not translate into large changes in allocations by region or country income level. With extreme poverty increasingly concentrated in conflict-affected and climate-vulnerable countries, prioritising fragility is a defensible strategic option. However, the question will be whether an aid programme dominated by humanitarian relief is able to contribute to reducing poverty in a sustainable way.

Endnotes

- 1 The comparison of spending plans with historical spending is not precise, as aid statistics are given on a calendar-year basis, while the spending plans are given in financial years. In addition, certain items that are included in statistics on past ODA spending are not included in the spending figures provided by FCDO – namely, non-departmental spending such as ODA-eligible research through UK Research and Innovation and the items listed under ‘Other contributors of UK ODA’ in Table 3 of UK Statistics on International Development. The available figures are, however, sufficient to give the broad picture of shifts in UK aid volumes and allocation. ↩

- 2 As above, the fall in this fiscal year involves a comparison of a financial year figure (2026-27) with a historical calendar year figure for 2025. Again, the financial year figure involves Departmental Expenditure Limits (DEL) spending only, while the calendar year spend includes non-DEL expenditure, which was £881.1 million in 2025. ↩

- 3 HM Treasury, ‘Spending Review 2025’, June 2025, Table 5.12, page 69 (viewed on 16 June 2026) ↩

- 4 Foreign, Commonwealth and Development Office, ‘ODA programme allocations 2026-27 – 2028-29’, annexed to Yvette Cooper, Foreign Secretary, Statement to Parliament, 19 March 2026 (viewed on 16 June 2026); Foreign, Commonwealth and Development Office, ‘Annual report and accounts 2024-2025’, 22 July 2025 (viewed on 16 June 2026) ↩

- 5 ‘In-donor refugee costs’ is a reporting category used when donors report their ODA spending to the OECD-DAC. Donors can report some of the cost of supporting refugees or asylum seekers for the first 12 months of their time in a donor country as ODA under this reporting category. OECD DAC has set out rules and clarifications for what costs donors can include. See previous ICAI reviews on the subject of IDRC: ‘UK aid to refugees in the UK’ (2023) and the subsequent Update (2023) ↩

- 6 For the historical figures, see Foreign, Commonwealth and Development Office, ‘Statistics on International Development: final UK ODA spend 2024’, September 2025, Table C1 (viewed on 16 June 2026) ↩

- 7 Yvette Cooper, Foreign Secretary, Statement to Parliament, 19 March 2026 (viewed on 16 June 2026) ↩

- 8 Independent Commission for Aid Impact, ‘Management of the official development assistance spending target: Information note’, July 2025, Box 4,

page 12 (viewed on 16 June 2026 ↩ - 9 Independent Commission for Aid Impact, ‘Management of the official development assistance spending target 2021-25’, March 2026 (viewed on 16 June 2026); Independent Commission for Aid Impact, ‘UK aid under pressure: a synthesis of ICAI findings from 2019 to 2023’, September 2023 (viewed on 16 June 2026) ↩

- 10 Organisation for Economic Co-operation and Development, ‘A historic decline in foreign aid: Preliminary 2025 ODA data’, April 2026 (viewed on 18 June 2026) ↩

- 11 World Bank data, ‘GDP per capita (current US$)’ (viewed on 19 June 2026) ↩

- 12 World Bank, ‘Malawi Poverty & Equity Brief’, October 2025 (viewed on 16 June 2026) ↩

- 13 Organisation for Economic Co-operation and Development, ‘Policy Brief – Cuts in official development assistance: OECD projects for 2025 and the near term’, June 2025 (viewed on 16 June 2026) ↩

- 14 Yvette Cooper, Foreign Secretary, Statement to Parliament, 19 March 2026 (viewed on 16 June 2026) ↩

- 15 See the FCDO programme, ‘Building Refugee Resilience and Inclusion in Turkey’ (viewed on 16 June 2026) ↩

- 16 Foreign, Commonwealth and Development Office, ‘Foreign Secretary warns the world cannot wait any longer to reopen the Strait of Hormuz, as food security crisis looms for countries already on the edge’, Press Release, 19 May 2026 (viewed on 25 June 2026) ↩

- 17 United Kingdom of Great Britain and Northern Ireland, and Ukraine, ‘One hundred year partnership agreement between the United Kingdom of Great Britain and Northern Ireland and Ukraine (CP 1277)’, 16 January 2025 (viewed on 16 June 2026 ↩

- 18 World Bank, ‘Ethiopia Poverty & Equity Brief’, October 2025 (viewed on 16 June 2026) ↩

- 19 See OCHA Financial Tracking Service, ‘Ethiopia Humanitarian Response Plan 2024’ (viewed on 16 June 2026) ↩

- 20 Independent Commission for Aid Impact, ‘UK aid’s international climate finance commitments: A rapid review’, February 2024, page 10 (viewed on 16 June 2026) ↩

- 21 Joe Lo, ‘UK halves Green Climate Fund contribution, as it spends more on security’, Climate Home News, 14 May 2026 (viewed on 29 June 2026) ↩

- 22 Foreign, Commonwealth and Development Office, ‘FCDO multi-year Official Development Assistance programme allocations 2026–2027 to 2028–2029: equality impact assessment’, 19 March 2026 (viewed on 25 June 2026) ↩

- 23 British International Investment, ‘Building Markets, Transforming Lives: 2026-2031 Strategy’, page 11 (viewed on 19 June 2026) ↩

- 24 Independent Commission for Aid Impact, ‘UK aid under pressure: a synthesis of ICAI findings from 2019 to 2023’, September 2023 (viewed on 16 June 2026) ↩