Management of the official development assistance spending target

Executive summary

The UK government has a target for official development assistance (ODA) spending across all its departments each year. By law this target is set at 0.7% of UK gross national income (GNI), but the government announced a reduction in spending to 0.5% of GNI from 2021 as a “temporary measure” in response to the economic effects of the COVID-19 pandemic. In February 2025, the Prime Minister announced a further reduction to 0.3% of GNI in 2027, to fund increased defence spending.

This review examines the principles and processes adopted to estimate the available ODA budget and to allocate it across UK government departments each year. It assesses whether those processes are a viable and effective way to ensure value for money relative to the UK’s objectives for development spending. It also assesses how the UK has interpreted the definition of ODA, particularly regarding spending on refugees and asylum seekers in the UK – known as in-donor refugee costs (IDRC) – and how that interpretation interacted with the allocation process and impacted on value for money.

The review covers the years 2021-22 to 2024-25 – a period of major disruption to the UK ODA budget – while also looking forward to the potential impact of changes announced at the 2025 Spending Review.

Key findings

The system for allocating ODA budgets across government during the review period was not always based on shared strategic priorities or evidence of value for money.

There has been no consistent overarching strategy or set of priorities for UK aid, and cross-government ODA management processes have often been narrowly focused on expenditure around the aid target, rather than delivery against an agreed set of results. This falls short when compared to the lessons from the National Audit Office’s work on a planning and spending framework that enables long-term value for money.

The combination of an ODA target set relative to GNI, the decision to treat this as both a ceiling and a floor, and the inclusion of policy-driven development spending and demand-driven asylum costs in a single target, undermined value for money.

There is an inherent challenge to budgetary planning and value for money from the decision by Parliament to set a target for spending relative to GNI, which is a moving target and by nature hard to forecast.

This challenge was compounded by the decision of successive governments, up to 2025, to treat the ODA spending target as an annual ceiling as well as a floor – that is, a figure that must be hit precisely without spending going above or below it – designating the Foreign, Commonwealth and Development Office (FCDO) as the spender and saver of last resort. This meant that FCDO had to adjust its budgets, often late in the financial year, to ensure that the target was met if there were fluctuations in GNI or another department’s costs unexpectedly increased.

The challenge was further compounded by including two different forms of spending together to meet a single target: policy-driven development spending aimed at reducing poverty in the poorest countries, and demand-driven spending on IDRC aimed at meeting the UK’s legal obligations to support asylum seekers. Under international aid rules, some of the costs associated with supporting refugees and asylum seekers who arrive in the UK qualify as ODA for the first year. This meant that any rise in IDRC automatically displaced funds from development spending overseas, regardless of value for money relative to the UK’s objectives.

As set out in past Independent Commission for Aid Impact (ICAI) reviews, despite the shortcomings of the system, FCDO was largely able to minimise the practical impact of these challenges before 2020 by careful forecasting and managing the timing of planned payments across calendar years.

However, this review covers a period characterised by less predictability in spending, in the face of volatile GNI and sharply rising IDRC, which peaked at 28% of the total aid budget in 2023. The measures required to hit the target left FCDO facing long periods of budgetary uncertainty, with real impacts on the quality of its programming and its ability to support global poverty reduction. This was a perverse outcome, given the intention of the International Development (Official Development Assistance Target) Act 2015, to protect UK aid flows in line with international commitments.

The system also weakened the incentive for the Home Office to manage its IDRC spending carefully, as any overspends were countered by reductions in the FCDO budget, rather than by use of other Home Office budgets.

Poor forecasting of IDRC by the Home Office also increased the disruption to other ODA spending, although there is evidence of improvement in recent years.

The UK has applied an expansive interpretation of IDRC, while staying broadly within international guidance, increasing the impact on wider ODA budgetary management.

Guidance agreed by the Organisation for Economic Cooperation and Development’s Development Assistance Committee (OECD-DAC) defines which categories of spending on assisting refugees may be reported as ODA. However, that guidance leaves donors a high degree of latitude in what they choose to report, including capping spend as a percentage of aid budgets, or reporting no spending at all, while technically remaining within the guidance.

ICAI’s benchmarking against two other donor countries, the Netherlands and Sweden, and against donor best practices collected by the OECD, found that the UK has consistently opted for the most expansive reporting option, contrary to the recommendation by the OECD to adopt a “conservative approach”. The UK also continued to use estimated imputations rather than actual costs for some areas of spending, including healthcare and education, raising risks of over-reporting.

Taken together, this expansive approach increased the pressure on the wider system of ODA allocation, increasing the risks to value for money.

Big differences in practices for reporting IDRC by donors across the OECD also undermined the coherence and comparability of international statistics for ODA.

The removal of FCDO’s role as spender and saver of last resort is a positive step but the implications for the overall approach to ODA are not yet clear.

From 2025-26, FCDO will be allocated an ODA budget in cash terms, giving greater budget stability and ability to plan for the medium term. The 2025 Spending Review reiterates the government’s commitment to bringing down IDRC, but assumes that they will continue to absorb approximately one-fifth of UK ODA.

While the removal of FCDO’s role as spender and saver of last resort is a welcome development, the 0.3% of GNI planning target continues to cover both development policy-driven spending and demand-driven asylum costs. The implication is that the outturn for ODA spending from 2027 onwards may be higher or lower than 0.3% depending on GNI growth and the government’s success in reducing IDRC. The ODA budgets allocated to FCDO will no longer be automatically adjusted upwards or downwards, so there would be no sudden in-year reductions of the kind that characterised earlier periods, but it is not clear whether the government would choose to make discretionary changes to budgets if outturns were to differ significantly from 0.3%.

New processes from 2025 for ODA allocation across departments may contribute to improved value for money but currently lack transparency and clear overarching objectives for the use of development funds.

FCDO was given a more active role in the allocation of ODA budgets in the 2025 Spending Review.

To enhance cross-government coordination, FCDO and the Treasury have re-established a ministerial-level cross-government Board of all the main ODA-spending departments, with a mandate to drive strategic coherence and value for money. The government has also stated an intention to ‘modernise’ the UK’s development cooperation. It will be important for the government to articulate this new vision as soon as possible, to provide a strategic framework for departments to make best use of reduced ODA budgets.

Recommendations

Recommendation 1: The UK should put in place a strategic, evidence-based, comprehensive and transparent approach to the allocation of ODA budgets across government departments, based on a viable framework for achieving long-term value for money.

Recommendation 2: The UK should confirm a permanent end to the FCDO’s role as spender and saver of last resort and ensure that any ODA spending target is no longer treated as both a ceiling and a floor.

Recommendation 3: The UK should take measures to increase the medium-term predictability of ODA allocations, for example by establishing multi-year rolling commitments.

Recommendation 4: The UK should separate the allocation, management and public reporting of in-donor refugee costs from other forms of ODA, in recognition of the distinct purpose and demand-driven nature of asylum support.

Recommendation 5: The UK should work with the OECD Development Assistance Committee and other OECD members to reduce the impact of different in-donor refugee cost reporting practices on the coherence and comparability of international ODA statistics.

1. Introduction

1.1 The UK government has a target for official development assistance (ODA, or ‘aid’) spending across departments each year. By law, the target is set at 0.7% of UK gross national income (GNI), reflecting a long standing UN aspiration to scale up global aid to this level. In recent years, however, the government has reduced the aid budget, first to 0.5% of GNI in 2021 as a “temporary measure” in response to the economic effects of the COVID-19 pandemic, and then to 0.3% in 2027, to fund increased defence spending.

1.2 This Independent Commission for Aid Impact (ICAI) review examines the principles and processes adopted to estimate the available ODA budget, and to allocate it across UK government departments each year. The review assesses whether those processes are a viable and effective way to ensure value for money relative to the UK’s objectives for development spending. Though remote from the frontline of aid delivery, these cross-government processes have impacted profoundly on the value for money of UK aid in the turbulent years since the COVID-19 pandemic.

1.3 The review also assesses how the UK has interpreted the definition of ODA, particularly regarding spending on refugees and asylum seekers in the UK – known as in-donor refugee costs (IDRC) – and how that interpretation interacted with the allocation process and affected value for money.

1.4 Achieving the ODA spending target each calendar year is challenging, for several reasons. First, there is an inherent challenge to budgetary planning and value for money from the decision by Parliament to set a target for spending relative to GNI, which is a moving target and by nature hard to forecast. Second, uniquely among donor countries, the UK defines its target as both an annual floor and an annual ceiling – that is, a figure that must be hit precisely without spending going above or below it. This involves managing significant levels of uncertainty. UK GNI is not known for certain until after the end of the year, and many items of ODA expenditure are difficult to predict.

1.5 Crucially, the UK government has also expected one single department, the Foreign, Commonwealth and Development Office (FCDO) to take on the ‘spender and saver of last resort’ role required of the former Department for International Development. ODA spending must therefore be carefully monitored by FCDO over the course of the year in response to emerging GNI projections and cross-government ODA spending estimates, with last-minute adjustments each December to hit the target to the required degree of precision. This meant that FCDO had to adjust its budgets, often late in the financial year, to ensure that the target was met if there were fluctuations in GNI or another department’s costs unexpectedly increased.

1.6 This approach is at odds with the need for “realistic and stable funding commitments” identified by the National Audit Office in its approach to frameworks for planning and spending to enable long-term value for money. It also varies from the way the Treasury otherwise discharges its responsibility to provide predictable budgets to spending ministries so that they may more easily deliver value for money.

1.7 Since the COVID-19 pandemic, the challenge of hitting a precise annual spending target has been made far more difficult by unprecedented levels of volatility, as a result of fluctuations in UK GNI during the pandemic and successive ODA budget reductions. The challenge was further compounded by including two different forms of spending together to meet a single target: policy-driven development spending aimed at reducing poverty in the poorest countries, and demand-driven spending on IDRC aimed at meeting the UK’s legal obligations to support asylum seekers. This meant that any rise in IDRC automatically displaced funds from development spending overseas, regardless of value for money relative to the UK’s objectives.

1.8 As set out in past reviews by ICAI – including ‘Management of the 0.7% ODA spending target’ (2020) and its update in 2021 – the processes worked reasonably well in years when the budgetary parameters were fairly predictable. However, from 2020 onwards, as conditions became more volatile, they began to present significant value for money risks.

1.9 This review continues the work of past reviews to cover the period from 2021-22 to 2024-25, while also looking forward at changes announced in the 2025 Spending Review. As a secondary issue, the review also revisits and assesses how the UK has interpreted the ODA definition – particularly in respect of refugee support costs, and whether this was an optimum approach to ensure value for money in ODA spending. It builds on ICAI’s 2023 review, ‘UK aid to refugees in the UK’, and its information note, ‘Management of the official development assistance spending target’, published in July 2025.

1.10 The review questions (see Table 1) address the systems and processes involved in allocating and managing ODA budgets across departments from a value for money perspective, the implications of how the UK defines its ODA target, and lessons for managing ODA spending in the current spending review period. In this context, value for money refers to the UK’s ability to allocate ODA budgets across departments and coordinate their spending in ways that support the achievement of a coherent set of objectives. ICAI’s approach to assessing value for money in this review draws substantially on National Audit Office guidance on effective cross-government planning and spending frameworks. The findings section of the report is structured under the review questions, and is followed by conclusions and recommendations.

Table 1: Review questions

| Review questions | |

|---|---|

| 1 | How effective were the systems and processes for allocating and managing the official development assistance (ODA) budget across government departments from 2021-22 to 2024-25, and did these create a viable framework to ensure value for money? |

| 2 | What has been the impact of the UK’s interpretation of the definition of official development assistance (ODA) from 2021-22 to 2024-25, in particular of in-donor refugee costs, and to what extent is this in line with international comparators? |

| 3 | What lessons could the UK adopt from its previous approaches to allocating and managing official development assistance (ODA) in the period covered by the 2025 Spending Review, to maximise long-term value for money and facilitate policy coherence on ODA across government? |

1.11 The review methodology involved a number of elements:

- A review of government strategic documents and policies.

- A mapping and analysis of the systems and processes for allocating, managing and coordinating ODA budgets.

- A review of past findings and recommendations by ICAI and other scrutiny bodies, and the government’s response.

- Financial analysis of cross-government ODA spending, including the management of past ODA budget reductions.

- Benchmarking of UK practices against those of other donors, especially the Netherlands and Sweden.

- Engagement with a range of stakeholders across ODA-spending departments, including FCDO, the Treasury, the Home Office and others, and with a range of external stakeholders.

Altogether, the methodology involved the collection and review of more than 680 documents, 37 interviews, and two roundtables with a total of 22 participants.

2. Background

2.1 This section of the report provides an introduction to key concepts, processes and trends in the cross-government management of official development assistance (ODA), to provide context for the analysis that follows. A more detailed description is available in ICAI’s July 2025 information note, ‘Management of the official development assistance spending target’.

The definition and purpose of ODA

2.2 The definition of ‘official development assistance’ is agreed internationally by the Organisation for Economic Cooperation and Development (OECD). The OECD’s Development Assistance Committee (DAC), consisting of 33 donor countries, agrees statistical standards for reporting ODA and publishes global aid statistics.

2.3 ODA is defined as aid by governments and official agencies to a list of ODA-eligible countries or via specified multilateral organisations, with the promotion of the economic development and welfare of developing countries as its main objective. This international definition is reflected in the UK’s International Development Act 2002, which provides the statutory authority for most ODA spending (although, significantly, not in-donor refugee costs).1 The Act also specifies that, when spending development assistance, the minister must be satisfied that it is “likely to contribute to a reduction in poverty”.2 This sets poverty reduction as the overarching purpose of UK aid, while leaving ministers discretion to determine how best to achieve it. A subsequent law from 2014 provides that, when spending development assistance under the International Development Act, the minister must also consider whether aid can be provided in ways that contribute to reducing gender inequality.3

The ODA spending target

2.4 In 1970, the UN General Assembly made a non-binding recommendation that donor countries should aim to provide development assistance at the level of 0.7% of their gross national income (GNI). The figure was based on modelling of the additional resources that developing countries would need to invest in national development in order to achieve a healthy growth rate, above what could be financed from domestic savings. While the modelling is now dated, the target has been retained, reflecting a collective aspiration to scale up investment in the UN Sustainable Development Goals.4

2.5 The UK first pledged to scale up towards the UN target at the 2005 G8 Summit in Gleneagles. Over the next eight years, it doubled its aid, reaching 0.7% in 2013, and enshrining the target in law two years later. The International Development (Official Development Assistance Target) Act 2015 imposes a duty to achieve the statutory 0.7% target and specifies that, if the target is missed in any given year, the government must explain to Parliament why it has been missed and what steps will be taken to ensure a return to 0.7% the following year. The Act specifies that this obligation to report to Parliament is the sole form of accountability attaching to the target.5

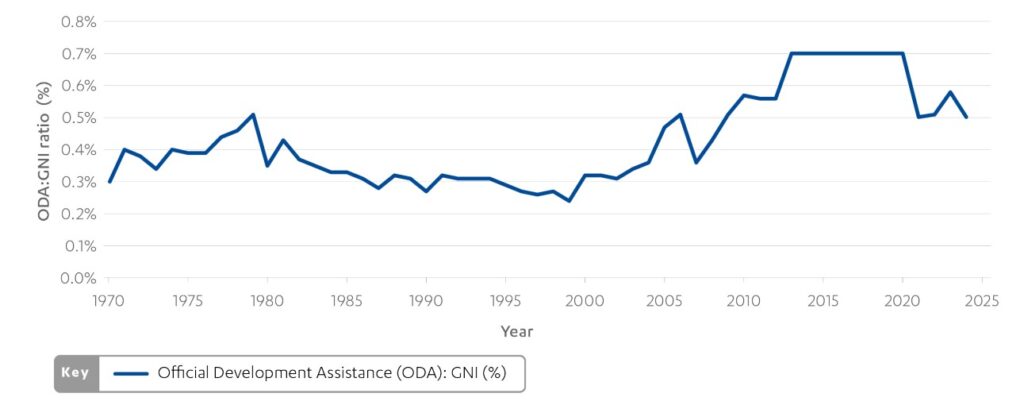

Figure 1: UK official development assistance (ODA) levels as a percentage of gross national income (GNI), 1970-2024

Line chart showing the ratio of UK development spending to GNI

Source: Foreign, Commonwealth and Development Office data in ‘Statistics on International Development: final UK ODA spend 2024’, and Foreign, Commonwealth and Development Office data in ‘Statistics on International Development: final UK ODA spend 2023’ (viewed on 15 December 2025)

Description: The line chart shows UK ODA as a percentage of GNI trending overall upwards between 0.36% and 0.5% until 1979, downwards to 0.24% in 1999, and then upwards to reach 0.7% between 2013 and 2020. In 2021, the line drops downwards to 0.5%, rises to 0.58% in 2023, and falls again to 0.5% in 2024.

2.6 As Figure 1 shows, the UK met the 0.7% target each year from 2013 to 2020. However, in 2021, the Foreign Secretary informed Parliament that the UK would spend only 0.5% as a temporary measure, pledging to return to 0.7% “when the fiscal situation allows”.6 The government set two fiscal tests for a return to 0.7%. Based on current economic forecasts, these are not expected to be met until at least 2030 7 leading to some debate about the legality of this course of action.8

2.7 On 25 February 2025, Prime Minister Keir Starmer announced that the UK would reduce its ODA budget from 0.5% to 0.3% of GNI in 2027,9 as part of a plan to increase UK defence spending. Since the 2025 Spending Review, the government has characterised the target as “equivalent to 0.3% of GNI”. We understand this to mean that it will set departmental ODA budgets in cash terms to meet 0.3% of the Office for Budget Responsibility’s forecast for GNI, rather than targeting a specific outturn. The government has signalled that the reduction will be accompanied by a process of ‘modernising’ UK aid, with a shift of focus towards providing expertise and mobilising other sources of development finance, rather than the direct funding of development projects.10

Allocation of ODA across departments

2.8 UK aid is currently spent by 18 UK government departments, plus the Scottish and Welsh governments and through various non-departmental channels.11 The primary means for allocating ODA budgets across departments is through spending reviews – periodic processes by which the government, led by the Treasury, sets departmental spending limits for areas of expenditure that are reasonably predictable. Spending reviews usually cover a three- or four-year period, although one-year processes are sometimes used. The process by which departments bid for and receive ODA budgets is described below in para 3.6 to 3.7. These budgets are further divided into ‘resource departmental expenditure limit’ for day-to-day operations, and ‘capital departmental expenditure limit’ for investments, such as loans, equity investments, capital injections into British International Investment (BII) and certain multilateral contributions.

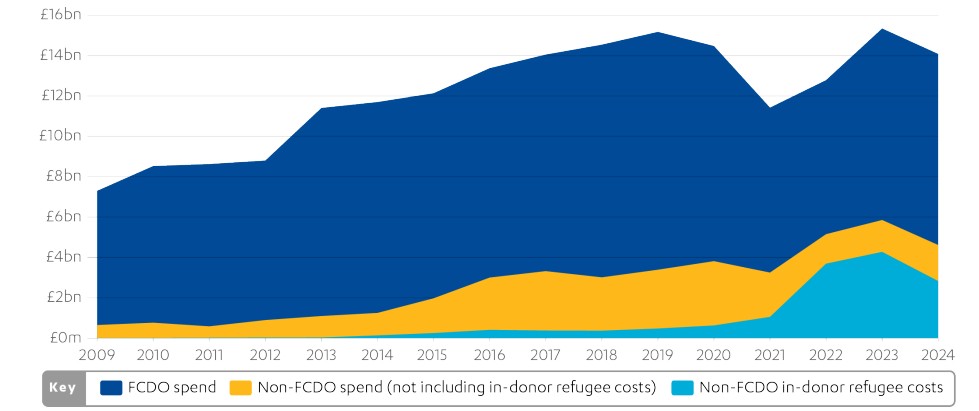

2.9 In the period from 2010 to 2014, the former Department for International Development (DFID) and Foreign and Commonwealth Office (FCO) – which later merged to become the Foreign, Commonwealth and Development Office (FCDO) – spent around 90% of total UK ODA.12 From 2015, that share steadily fell, reaching a low of 60% in 2022, before returning to 67% in 2024. There were a number of reasons for this fall, including a rise in UK international climate finance (aid given to support countries to respond or adapt to climate change), ODA-financed research expenditure and, above all, spending on refugees in the UK – all items that involve significant spending by departments other than FCDO.

Figure 2: The growing share of UK aid spent on domestic refugee costs

Stacked area chart showing how aid spending is split between FCDO and other departments between 2009-24 (FCDO spend includes its predecessor departments)

Source: Foreign, Commonwealth and Development Office data in ‘Statistics on International Development’, various years (viewed on 15 December 2025)

Description: The chart shows how FCDO (and its predecessor departments’) spending increases steadily to a high point between 2013 and 2019, drops sharply in 2021, then rises again in 2023. Non-FCDO spending (excluding in-donor refugee costs) grows slowly at first, increases more quickly around 2014-17, peaking in 2020 before falling sharply. In-donor refugee costs are very low until 2015, rise modestly to 2021, spike in 2022 and 2023, then drop in 2024. Overall, total aid spending climbs from 2009 to 2019, declines in 2020-21, rises again in 2022-23, and dips slightly in 2024, with recent changes driven mainly by shifts in in-donor refugee costs.

The rise of in-donor refugee costs

2.10 Not all UK ODA is allocated through spending reviews. UK government spending on refugees and asylum seekers in the UK is determined by statutory entitlements,13 and varies year on year according to arrival numbers and variable cost factors. The international ODA definition includes certain spending to support refugees and asylum seekers during their first year in the UK, including on accommodation, food, healthcare and children’s education. This category of ODA expenditure is known as ‘in-donor refugee costs’ (IDRC). These costs can vary significantly across years. Under the UK government rules that applied throughout the review period, IDRC is deducted from FCDO’s ODA allocation, to ensure that the fixed planning target for spending is achieved. This meant that any rise in IDRC automatically displaced funds from development spending overseas, regardless of value for money relative to the UK’s objectives.

2.11 IDRC have risen dramatically in recent years (see Figure 2). This has mainly been due to a steep rise in the costs per head of supporting refugees and asylum seekers. Increased arrivals of refugees and asylum seekers, including Afghan citizens following the August 2021 fall of Kabul to the Taliban and Ukrainians following the 2022 full-scale Russian invasion, also contributed to an increased backlog of undecided asylum claims, and more people being entitled to support. A shortage of accommodation has led the Home Office to house refugees and asylum seekers in rented hotels. At one stage, in October 2022, rental contracts in over 400 hotels were costing £6.8 million per day.14 As a consequence, IDRC rose sharply from £628 million in 2020 to £4.3 billion in 2023, when they absorbed 27.9% of the aid budget, before falling back to £2.8 billion in 2024 (20.1%). When combined with aid budget reductions, the rise in IDRC caused all other aid to fall by £5.6 billion, or 38%, in 2022, compared to its 2019 peak, with further falls projected as the aid budget is progressively reduced to 0.3%.

2.12 ICAI calculations, based on figures published in the 2025 Spending Review, show that the government projects only modest reductions in IDRC in the coming years, suggesting that IDRC will continue to absorb approximately one-fifth of the UK aid budget. With the ODA planning target falling to 0.3% of GNI in 2027, this will leave the UK aid available for other purposes at just 0.24% of GNI – the lowest level relative to national income in more than 50 years of UK ODA statistics, matched only in 1999.15

2.13 The UK’s approach to calculating and reporting IDRC – assessed under the second review question from paragraph 3.7 onwards – has also changed considerably over the years, contributing to the increase in refugee costs reported by the UK as ODA. IDRC was first included in the international ODA definition in 1988, on the basis that support for refugees is a form of humanitarian aid, wherever provided. This was a controversial decision, as the funds are not transferred to a developing country, and the UK initially declined to report any ODA spending in this category. The UK only began reporting IDRC in 2010, to bring its ODA statistics in line with international practice, and even then reported relatively minor amounts – £12 million in 2010, rising to £135 million in 2014.16 Since 2010, government methods for calculating IDRC have become much broader, capturing not only the costs of resettling refugees in the UK, but also a larger share of the first-year support costs for resettled refugees and asylum seekers, as well as the Homes for Ukraine scheme. Past ICAI reviews have found that, while UK reporting practices are in accord with guidance from the OECD-DAC, they are now more expansive than those of many other donors.17

3. Findings

3.1 The findings of the review are organised under the three review questions set out in Table 1. They address respectively the processes by which official development assistance (ODA) budgets are allocated and managed across government, the impact of the UK’s interpretation of the definition of ODA (including in-donor refugee costs), and lessons from the review period for implementation of the 2025 Spending Review.

How effective were the systems and processes for allocating and managing the ODA budget across government departments from 2021-22 to 2024-25, and did these create a viable framework to ensure value for money?

The allocation of ODA budgets across government is not based on a shared set of priorities or results for UK development cooperation

3.2 According to National Audit Office (NAO) lessons on cross-government planning and spending frameworks,18 one of the eight key lessons on the allocation and coordination of spending across government departments is the importance of a shared set of objectives. This has not generally been the case for UK ODA over the review period, for a number of reasons.

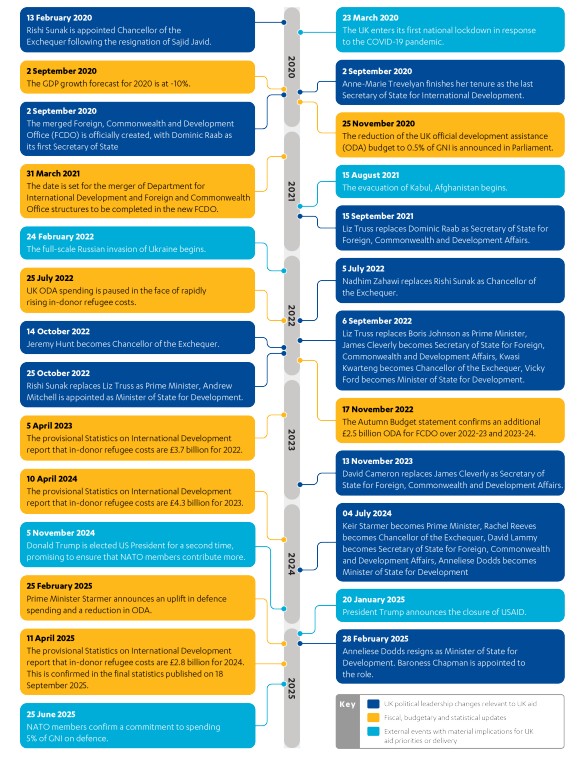

3.3 The UK has lacked a clear or stable set of overarching objectives for aid. The uncertain context that followed the onset of the COVID-19 pandemic was compounded by rapid turnover across the great offices of state (see the timeline in Figure 3). Changes in prime ministers, chancellors of the exchequer, foreign secretaries and home secretaries through 2021 and 2022 led to shifts in direction and priorities for UK aid. Decision-making often took the form of public announcements, which were accorded lower importance following ministerial changes but rarely formally withdrawn, making it difficult to judge exactly what the priorities were at any given time. An International Development Strategy was released in May 2022 (the first in seven years), only to be followed by a number of other strategies in quick succession, including the 2023 Integrated Review Refresh, a 2023 progress update on the 2022 International Development Strategy, and a new International Development White Paper in November 2023. These varied in the extent to which they purported to apply to UK development cooperation as a whole or were based on a shared vision across government.19

3.4 Overall, the review period was marked by a lack of consistent priorities or intended results for UK aid as a whole. This makes it difficult to conclude that there was a compelling, results–based rationale for the allocation of ODA budgets across departments, in accordance with the statutory objectives of promoting poverty reduction and reducing gender inequality. We have not been able to identify any structured process by which aggregate UK aid expenditure was aligned behind a consistent and explicit set of international development priorities.

3.5 As ICAI has previously noted, in the absence of a clear strategy to guide the allocation of the aid budget, the ODA spending target, and the challenges of applying it in a period of such volatility, led to major shifts in the utilisation of aid that did not reflect any stated strategy or priority.20

Figure 3: Timeline of change 2020-25

The allocation of ODA budgets under past spending reviews lacked clear criteria for enabling long-term value for money

3.6 The UK has lacked a system for allocating aid budgets across departments in ways that align with overarching objectives or results targets. During Spending Reviews, UK government departments have been given an opportunity to bid for a share of the ODA budget. Bids are assessed by the Treasury and used to guide ODA allocations. Departments are required to demonstrate that their proposed ODA programmes align with government policy and that they have the capacity to use the funds effectively.

3.7 The process provides the Treasury with some evidence on each department’s intended use of the ODA budget, how it contributes to the government’s objectives, and its experience with managing aid programmes of that type. However, we find that the allocation approach does not represent an adequate framework for maximising long-term value for money. The NAO has shared a set of lessons that can be learned from its work on how the government can use its planning and spending framework to enable value for money. We used that as a reference point for an assessment of whether the ODA allocation process is focused on enabling long-term value for money.21 We found a series of factors (summarised in Table 2 and presented in full in Annex 3) that work against long-term value for money in cross-government ODA management, including the lack of a clear strategy or results areas, inadequate governance arrangements, lack of clear criteria for balancing the priorities and interests of different departments, and a lack of process for monitoring results at the cross-government level. In the absence of elements such as these, allocations have tended to reflect historical patterns among departments22, the bargaining power of respective ministers, and short-term pragmatic decision-making in response to falling budgets and rising in-donor refugee costs (IDRC).

3.8 Furthermore, whatever value for money considerations guided spending reviews, their allocations have been repeatedly disrupted or revised following changes in the wider context. During the first year of the pandemic, in 2020, a fall in UK gross national income (GNI) led to major in-year reductions to the ODA budget. A cross-government Star Chamber (an ad hoc committee of senior ministers led by the Treasury) was established to revise ODA allocations across departments. Two years later, allocations under the 2021 Spending Review were revisited to reflect the rapid rise in IDRC.

Table 2: Reflecting on the National Audit Office (NAO) lessons on long-term value for money

| Theme | Lessons to maximise long-term value for money (NAO) | Examples of issues identified by ICAI |

|---|---|---|

| Joined-up planning and governance | Plan and manage spending, risks and delivery against common objectives across organisational boundaries. | Lack of an overarching ODA strategy or outcomes framework, and limited strategic oversight by the ODA Board. |

| Prioritisation | Establish clear whole-of-government and departmental priorities and use them to guide affordable spending choices. | No consistent cross-government approach to prioritising ODA or balancing departmental and nondepartmental ODA. |

| Data and evidence | Base decisions on good evidence about efficacy, costs and risks, particularly when working at speed. | Limited evidence of a portfolio approach to inform allocative decisions. |

| Monitoring and evaluating | Monitor costs, performance and risk levels; build in rigorous in-flight and post-hoc evaluation to enable learning. | No shared cross-government metrics for assessing ODA value for money. |

| Taking a longterm view | Take a long-term perspective, consider future scenarios, and balance short-term objectives with sustainability and resilience. | Short spending review cycles constrained long-term planning. |

| Funding commitment | Set clear short-, medium- and long-term objectives underpinned by realistic and stable funding commitments, especially when working with local and private sector partners. | Reduced focus on value for money due to pressure to meet ODA spending targets. |

| Realism | Ensure realistic assessments of deliverability, cost, timelines and uncertainty when committing funding. | Unrealistic budget assumptions resulted in material underspends. |

| Transparency | Be transparent about objectives, plans, spending choices, risks and performance. | Transparency varied significantly across departments. |

Cross-government coordination of ODA has focused on meeting the annual spending target, rather than promoting value for money

3.9 In the absence of an overarching strategy for UK aid, cross-government coordination of ODA has been mainly focused on meeting the spending target. The process of meeting the target has been led by the Foreign, Commonwealth and Development Office (FCDO) in its capacity as spender and saver of last resort, and geared to providing it with timely and reliable reporting on and forecasting of other departments’ ODA spending over the course of each calendar year. This allowed FCDO to adjust its own spending accordingly, to ensure that the UK met, but did not exceed, the ODA budget.

3.10 To assist FCDO with managing processes to hit the target, a senior officials’ group has operated since 2015 to coordinate the ODA spending target. This has, from time to time, been supported by a junior officials’ group and other ad hoc structures, such as a sub-committee on in-donor refugee costs. A ministerial-level cross-government ODA Board has also operated at various points to provide oversight. However, these coordination mechanisms have been focused on hitting the spending target. They have not sought to promote coherence in the delivery of cross-government aid strategies or priorities, or to drive long-term value for money across the aid budget. Since the 2024 election, the ODA Board has been relaunched, as discussed further in para 3.58.

3.11 As a consequence, beyond the management of spending to hit the annual planning target, there has been no cross-government structure tasked with ensuring overall value for money in the allocation and management of the UK aid budget. This contrasts with some well-developed coordination mechanisms in specific thematic areas. For example, there has been a well-developed architecture for the Conflict, Stability and Security Fund (CSSF) and for its successor, the UK Integrated Security Fund (ISF), which coordinates the use of ODA on conflict and stability issues, in accordance with priorities set by the National Security Council. UK international climate finance (ICF) also has structures and processes that coordinate the contributions of the responsible departments (FCDO, the Department for Energy Security and Net Zero and its predecessors, and the Department for Environment, Food and Rural Affairs) to shared results areas.

3.12 As previous ICAI reports have found, the processes for meeting the spending target were generally well managed by FCDO, enabling the UK to hold to its planning target for ODA spending under even the most difficult conditions, but the value for money risks of hitting a specific spending target increased over time as conditions become more volatile (see Box 1).

Box 1: Managing the ODA spending figure

The 2020 ICAI review, ‘Management of the 0.7% ODA spending target’, examined the management

and coordination process for achieving the 0.7% statutory spending target. A set of cross-government mechanisms emerged after the 2015 Spending Review, including a senior officials’ group with overall responsibility for overseeing the ODA target. The Department for International Development (DFID), and later FCDO, were given the role of spender and saver of last resort and required to adjust their budgets to offset shifts in UK GNI and any variations in expenditure by other departments. This was a pragmatic choice. As the largest spender of ODA, FCDO is better placed to adjust its expenditure than other departments.

Over the course of the calendar year, FCDO would obtain regular ODA spending reports and forecasts from other departments, track non-departmental spend (ODA expenditure that does not fall within any department’s budget) and monitor UK GNI forecasts. The Supplementary Estimates process was used where needed to reallocate budgets between departments. Up until the 2021 Spending Review, the Treasury required departments other than DFID to spend most of their ODA allocation (eventually set at 80%) in the first three quarters of the year. ODA spending was then largely paused during December, allowing FCDO to adjust its own spending, principally by shifting the timing of certain payments to multilateral organisations across the end of the year, to hit the target.

The 2020 ICAI review concluded that this system for managing the ODA spending target was well suited to handling typical levels of variability in GNI and ODA spending. However, the much higher levels of volatility experienced from 2020 onwards made the task much more fraught. While FCDO officials succeeded in hitting the planning target, the measures they were required to take became more drastic in the face of this increased volatility. In these circumstances, the UK’s system for managing its ODA spending to hit a specific planning target began to pose major value for money risks.

3.13 In the face of such volatility, efforts to hit an inflexible spending figure became highly disruptive of the UK aid programme. FCDO was left facing lengthy periods of budgetary uncertainty, hampering forward planning and forcing it to make rapid, in-year adjustments to its expenditure. As well as the heavy management burden, this has real impacts on the quality of the department’s programming. In a written response to the Chair of the Public Accounts Committee, FCDO described impacts on the ability to reach priority populations with humanitarian support, basic services, and assistance informing sexual and reproductive health choices; to support improvements in governance; and to monitor and evaluate programmes effectively.23 The disruption to programme planning is a perverse outcome given the respective intentions of the UN aid target and the International Development Act 2015 to increase and maintain global and UK aid flows as a percentage of national income.

3.14 The options available for managing ODA spending against a fixed planning target have been further constrained by the UK’s practice of making multiannual funding commitments for specific parts of the aid programme. Fixed spending commitments in defined areas have had unintended consequences as the aid budget has fallen, resulting in reduction of other expenditure within an overall reduced allocation.

3.15 Over the review period, this has been particularly true of the commitment to spend £11.6 billion in ICF over the period from 2020-21 to 2025-26. As described in ICAI’s 2024 review of UK aid’s ICF commitments, this commitment was backloaded towards the final year of the five-year period.24 At the time of writing, the UK is now considering what ICF target to set for the next five years.

3.16 Within the ODA budget, fixed allocations for operating costs – resource departmental expenditure limit (RDEL) and capital departmental expenditure limit (CDEL) – have further compounded the volatility challenge for FCDO as spender and saver of last resort. The Treasury sets the ratio between CDEL and RDEL in order to protect long-term capital investment from being raided for short-term operational needs. Capital expenditure within the UK aid programme includes loans and equity investments, capital contributions to British International Investment (BII) and financial contributions to multilateral organisations that create a financial asset for the UK (such as paid-in capital to the World Bank). The breadth of options affords FCDO some scope for aligning CDEL allocations with departmental priorities. Nonetheless, this separation of the budget does constrain FCDO’s options in allocating resources – particularly when, as in 2024 (see para 3.24 below), it is required to make unexpected reductions in its CDEL allocation.

The government’s interpretation of the ODA spending target as both an annual floor and an annual ceiling has left UK aid highly vulnerable to budget volatility

3.17 It was the government’s choice to treat its 0.7% ODA spending commitment as a strict ceiling every year, as well as a floor. This is not mandated by the International Development Act 2015, which simply requires that the 0.7% UN target be met in each calendar year.25 Even when the aid budget was temporarily reduced to 0.5%, the government still opted to treat it as both an annual floor and an annual ceiling, despite the fact that 0.5% was merely an administrative or planning target, or budget ambition (making use of the provision in the Act allowing the government to explain to Parliament why the 0.7% target has been missed).

3.18 In the years between 2015 and 2019, FCDO was able to manage this variability by changing the timing of planned multilateral payments across the end of the calendar year. This did not significantly affect its own financial year planning, nor the work of the multilateral organisations in question. ICAI therefore concluded in its 2020 review that the arrangements did not represent a risk to the value for money of UK aid. However, from 2020 onwards, as conditions became more volatile, FCDO was forced to take more drastic measures to achieve the annual planning target. These included in-year programme cuts, spending freezes and delayed budget decisions. The measures have entailed significant compromises to the value for money of UK aid, resulting in large, unplanned diversions of aid away from FCDO’s apparent priorities for development cooperation. The Organisation for Economic Cooperation and Development’s Development Assistance Committee (OECD-DAC) commented in its 2020 Peer Review on the UK’s rigid interpretation of its aid target, noting: “The United Kingdom’s legislative requirement to spend 0.7% of GNI as ODA each year is countered by public and political pressure not to exceed that target, resulting in tightly bound annual spending margins. The United Kingdom could draw on the experience of other DAC members who use a range of budget mechanisms to smooth ODA budgets and expenditure over several years, mitigating the impact of annual fluctuations.”26

3.19 In its 2023 mid-term review, the OECD-DAC noted “limited progress” with ODA levels, commenting that: “management of the ODA/GNI targets as both a maximum and minimum, the downward pressure on the ODA budget, larger share of ODA spent at home, and the impact of the FCDO merger on staffing, have undermined transparency and the quality of programming”.27

The UK’s interpretation of its aid target as an annual floor and ceiling, and its designation of FCDO as spender and saver of last resort, means that any rise in IDRC takes ODA funding away from other uses.

3.19 As a result of the UK’s unique approach of treating the ODA target as both a floor and a ceiling, every pound of ODA allocated for IDRC in the UK automatically displaces a pound which could be spent on development overseas. This was the inevitable consequence of including two different forms of spending together to meet a single target. Bringing together policy-driven development spending aimed at reducing poverty in the poorest countries, and demand-driven spending on IDRC aimed at meeting the UK’s legal obligations to support asylum seekers, meant that FCDO, in its capacity as spender and saver of last resort, would always have to adjust its budgets downwards in response to rising IDRC.

3.20 As noted on the OECD-DAC website, most donors report that IDRC is “additional to the rest of their ODA programmes”.28 The UK chooses to offset IDRC with cutbacks in funding for global development and poverty reduction. ICAI’s 2023 review of UK aid to refugees in the UK noted that soaring IDRC caused such disruption to the UK aid programme that a decision was taken in July 2022 to pause all “non-essential” ODA spending for four months.29 Faced with an overspend risk of up to £1.15 billion from increased spending on IDRC, in July 2022 the Treasury called for a pause in all but essential ODA spending.30 The pause lasted until November 2022.

3.22 The Treasury did permit FCDO to exceed the 0.5% GNI budget figure by spending an additional £2.5 billion across financial years 2022-23 and 2023-24, but this one-off measure offset only a minor share of the nearly £8 billion in IDRC in those two years. While IDRC fell slightly in 2024, to £2.8 billion, it continued to displace significant amounts of other ODA spending, leading to in-year reductions to FCDO’s budget of £1.7 billion in 2022-23.31 Overall, ODA allocations under spending reviews since 2021 have varied so greatly from eventual ODA expenditure that any initial value for money considerations have ceased to be applicable.

3.23 The actions required to hit the 0.5% planning target in 2024 show just how dysfunctional the system became in the face of sharply rising IDRC. In July 2024, FCDO agreed with the Treasury to give up £991 million from its CDEL allocation under the 2021 Spending Review, after IDRC had reached an unprecedented £4.3 billion in 2023, equivalent to 28% of the total aid budget.32 By November 2024, tracking of UK GNI and other departments’ ODA spending forecasts suggested that FCDO would require additional funds (from those previously given up) to avoid undershooting the 0.5% target. The Treasury therefore agreed to make an additional £400 million available in December 2024. Even then, however, the level of uncertainty in the forecasts was such that FCDO was required at very short notice to reprofile £135 million in bilateral aid into the first quarter of 2025, to avoid overshooting the figure.

3.24 It is notable that there has never been an explicit government decision to prioritise IDRC over other aid spending. The Home Office Annual Report and Accounts for 2023-24 and 2022-23 both refer to “an increase in Official Development Assistance (ODA) funding to help mitigate pressures arising from these activities”. The UK’s decision to fully implement international OECD-DAC guidance to count IDRC as ODA, combined with the UK’s rigid interpretation of the spending target as both a ceiling and a floor, meant that ballooning IDRC automatically displaced spending on aid overseas pound-for-pound. Past ICAI reviews have noted that using resources on refugees in the UK, at the expense of crisis zones and refugee-hosting countries in the Global South, is both poor value for money and contrary to the objective of minimising secondary displacement into Europe and the UK.33

3.25 Moreover, the resources spent on IDRC did not represent value for money by any of the usual standards set for UK aid. The International Development Act 2002 sets poverty reduction as the underlying purpose of UK aid, alongside the reduction of gender inequality. ICAI has found no evidence that these objectives are advanced through the spending of ODA on IDRC. The 2023 ICAI review of UK aid to refugees in the UK found that ODA spent on IDRC was “not contributing to any of the priorities set out in the UK government’s International Development Strategy, published in May 2022”.34 Nor was there any assessment of how an expansive interpretation of IDRC affected the UK government’s ability to meet these legislative requirements to advance poverty reduction and gender equality. Rather, spending on IDRC has been based solely on its own separate purpose, to fulfil the UK’s statutory obligations to support asylum seekers.

3.26 Global crises have only intensified since 2023, with the situations in Gaza, Sudan and other countries requiring extensive humanitarian action. Yet in 2024, 20.1% (£2.8 billion) of UK ODA was spent on IDRC – £1 billion more than was spent on humanitarian aid.

3.27 Treasury documents indicate that the Home Office anticipates IDRC at £2.1 billion for the financial year 2025-26. This is less than in the previous three years, but still far above historical levels. At the same time, FCDO’s aid spending will fall from £9.3 billion in 2024-25 to £8.7 billion in 2025-26. In the context of the scaling down of ODA spending towards 0.3% in 2027, these figures show that the UK’s IDRC continues to significantly reduce the resources available to support developing countries.

3.28 The overall effect of this unprecedented volatility for ODA from IDRC, has been to conceal a reduction in ODA since 2021 (excluding IDRC) by instead giving the impression that the UK’s ODA budget as a total allocation steadily rose year on year between 2021 and 2023.35

The government’s management of the aid target has weakened the incentive for the Home Office to manage its in-donor refugee costs spending carefully to enable long-term value for money

3.29 The Home Office’s ability to charge an uncapped level of IDRC to the ODA budget has not encouraged long-term planning to secure improvements in value for money. There has, as a consequence, been serious and sustained criticism of the Home Office’s management of IDRC. Most recently, an October 2025 Home Affairs Committee report found that the Home Office’s response to the asylum accommodation crisis had focused on “high-risk, poorly planned policy solutions”, which “allowed costs to spiral” and “wasted considerable amounts of taxpayers’ money”.36 Its failures included poor procurement planning, systematic failures in management and oversight, and inadequate cost controls and budgeting. This closely mirrors ICAI’s conclusions from the rapid review in 2023, which found a range of poor procurement and contract management practices regarding large accommodation contracts.37

3.30 Consequently, the UK’s IDRC per refugee/asylum seeker is double or triple that of other DAC donors, at over $25,600 across 2022 and 2023. The mean IDRC per head across 31 DAC countries was $6,100. In the same period.38 The UK reports the highest cost per head, with the second-highest, Ireland, over $5,000 less, at $19,400.

3.31 As noted by ICAI in 2023, there is “less incentive from a financial perspective for the Home Office to reduce the backlog and long processing time for asylum applications since much of the resulting cost is borne by the aid budget”.39 Home Office officials noted in interviews for this review that they were focused on meeting their statutory obligations to refugees and asylum seekers, and any impact on other uses of UK aid was outside their control. This confirms the findings of ICAI’s 2023 review, which noted that the Home Office was not required to finance the rising costs of hotel accommodation through reductions elsewhere in its budget.

3.32 The Home Office has made some progress in reducing the number of asylum seekers accommodated in hotels, but this has had only limited impact on total spending on IDRC. The number of asylum seekers in hotel accommodation fell during the review period, from 45,753 at the end of 2022 to 38,054 at the end of 2024 – although this decline appears to have slowed, with 36,273 still in hotel accommodation as of 30 September 2025. A 2024 NAO investigation noted that the shift to “large sites” (such as former military sites, barges and unused office buildings) could in fact cost more than the use of hotels. This suggests that the pledge to end the use of hotels by 2029 may not necessarily result in savings to the UK aid budget.40 Poor forecasting of IDRC, although improved recently, has compounded the disruption of UK aid.

Poor-quality and volatile Home Office forecasting has added to the risks to UK aid posed by in-donor refugee costs spending

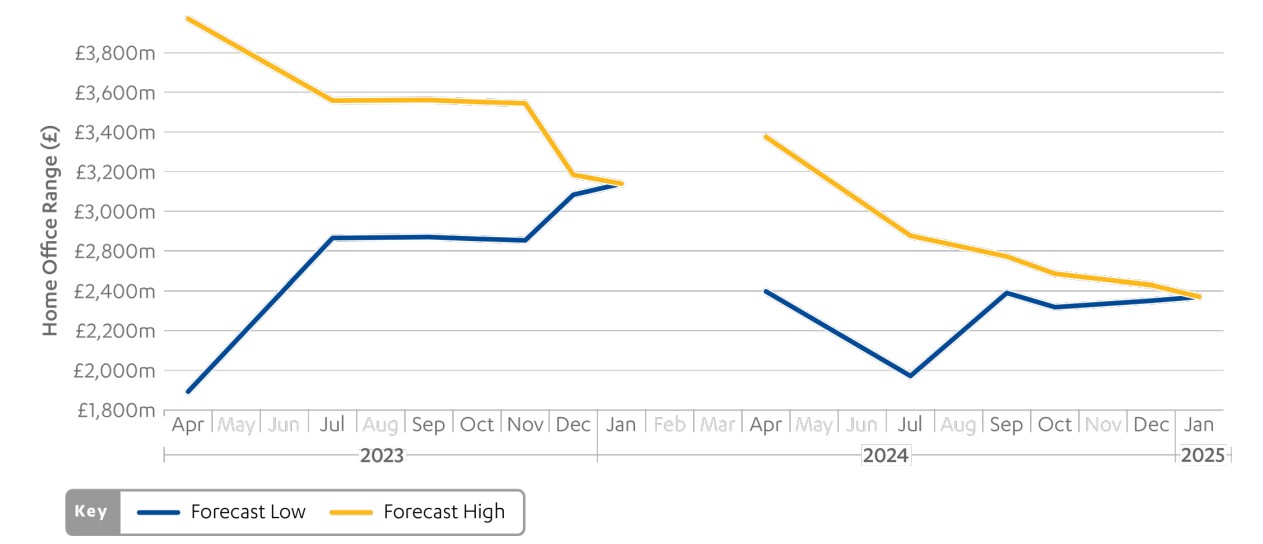

3.33 The 2023 ICAI rapid review noted that, following a pause on FCDO spending in 2022 in the face of rapidly rising IDRC, the Home Office “was unable, until almost the end of 2022, to predict with any certainty how much of that year’s ODA budget it would spend on refugees and asylum seekers”.41 Despite efforts by FCDO over the review period to encourage better forecasting, there continued to be wide variations between low-case and high-case projections from the Home Office in the early months of the year, which gradually narrowed towards year end. As Figure 4 shows, forecasting improved in 2024, but the variation between high- and low-case projections remained over £500 million into July 2024. Given that the resettlement schemes that had accounted for much of the initial rise in IDRC spend had exceeded the 12-month ODA-eligibility window by 2024, the overestimates provided by the Home Office in the first half of 2024 could likely have been avoided. One consequence was that FCDO was required to hold back a substantial share of its allocated ODA budget for much of the year, to allow for uncertainties in the Home Office’s IDRC forecasts.

Figure 4: Home Office forecasting of in-donor refugee costs in 2023 and 2024

Line graphs showing variations in forecasts for in-donor refugee costs by the Home Office between 2023 and 2024 (no data was provided for the months shaded in grey)

Source: Home Office, ‘Home Office ODA monitoring 2023’, 2024, unpublished; Home Office, ‘Home Office ODA monitoring 2024’, 2025, unpublished; Foreign, Commonwealth and Development Office, Home Office and Treasury, ‘ODA Board in-donor refugee costs ODA management discussion paper’, unpublished

Description: Forecasts for Home Office in-donor refugee costs changed substantially over time, indicating a high degree of uncertainty in expected spending. In both 2023 and 2024, estimates were revised sharply during the year, with large shifts in both the level of forecast costs and the range between higher and lower projections. This volatility suggests that initial forecasts provide a limited guide to eventual costs, with spending expectations only stabilising much later as forecasts become more precise. Overall, the data highlights the difficulty the Home Office faces in accurately predicting in-donor refugee costs over longer time horizons.

The lack of transparency in reporting of IDRC has exacerbated the challenge of cost management by the Home Office

3.34 Poor transparency and limited independent scrutiny in the management of IDRC have exacerbated disruption to other UK aid. In 2023, ICAI found that the UK had provided more information to the OECD-DAC on its methodology for calculating IDRC than most other donors, but that this was a low bar.42 This relative transparency does not, however, extend to the detail of the Home Office’s procurement and management of accommodation and other support services.43 The Home Affairs Committee and the Public Accounts Committee have recommended that the Home Office develop clear plans to reduce the costly and widespread use of hotels. The October 2025 report by the Home Affairs Committee noted that the Independent Chief Inspector of Borders and Immigration (ICIBI) plays an essential scrutiny role in the delivery of asylum accommodation.44 However, ICIBI has not had access to Home Office commercial contracts, which reduces its ability to scrutinise this area of expenditure. There is very little information in the public domain on the terms of the contracts established by the Home Office or the key performance indicators used to scrutinise the service providers.45

3.35 The lack of published and accessible data on IDRC makes external review and scrutiny especially difficult, and dilutes the incentive to drive down costs. Transparency of IDRC reporting varies across the responsible departments, with the Home Office identified as the least transparent department in the Publish What You Fund review of October 2025.46 In fact, as compared to the previous assessment in 2020, the Home Office had become less transparent in four out of five reporting areas.47 Moreover, the Home Office had published no 2024-25 updates or information on its planned activities in future years. This lack of transparency is a particular concern in the context of ongoing reductions in the UK aid budget to the equivalent of 0.3% of GNI by 2027, which requires important decisions to be made about how to allocate a decreasing aid budget.

Table 3: Publish What You Fund ratings on transparency among UK ODA-spending departments (excluding FCDO)

| Department | International or domestic spender | Overall performance | Performance indicator |

|---|---|---|---|

| Department for Education (DfE) | Domestic (local authority exclusions applied) | Progressed | |

| Department for Energy Security and Net Zero (DESNZ) | International | Progressed | |

| Department for Environment, Food and Rural Affairs (Defra) | International | Progressed | |

| Department for Science, Innovation and Technology (DSIT) | International | Maintained | |

| Department for Work and Pensions (DWP) | Domestic (local authority exclusions applied) | Progressed | |

| Department of Health and Social Care (DHSC) | International (with some domestic, not through local authorities) | Progressed | |

| Home Office (HO) | Domestic (not through local authorities) | Decreased | |

| Integrated Security Fund (ISF) | International | Progressed | |

| Ministry of Housing, Communities and Local Government (MHCLG) | Domestic (local authority exclusions applied) | Progressed |

Source: Publish What You Fund, ‘Progress and Gaps: Transparency of UK Aid Beyond the FCDO’, October 2025, page 12 (viewed on 15 December 2025)

What has been the impact of the UK’s interpretation of the definition of ODA from 2021-22 to 2024-25, in particular of in-donor refugee costs, and to what extent is this in line with international comparators?

The permissive nature of the OECD-DAC guidelines leaves donors a high degree of latitude in reporting their IDRC

3.36 The OECD-DAC sets the statistical standards for ODA reporting. DAC first introduced specific guidance on IDRC in its Statistical Reporting Directives in 1988 (see Box 2 on why IDRC came to be scored as ODA).

3.37 Its rules on calculating and reporting IDRC are relatively permissive, given diverse practices across donors which see DAC members operating at different levels along a spectrum of interpretations of the 2017 Clarifications on reporting. More detail on the spectrum of interpretation can be found in Annex 4. As discussed in para 2.13 above, the inclusion of IDRC in the international ODA definition has always been controversial, and there has been discussion in the OECD-DAC of the risks that sharp rises in IDRC pose to the credibility and integrity of international ODA statistics.

Box 2: Why in-donor refugee costs came to be scored as ODA

The OECD-DAC first introduced specific guidance on IDRC in its Statistical Reporting Directives in 1988. Members agreed that temporary costs for refugees and asylum seekers in donor countries could be counted as ODA, recognising that the financial burden of hosting refugees is a form of humanitarian support. This arose because DAC members wanted to account for the real cost of hosting refugees from developing countries, akin to providing humanitarian support abroad. The logic was that if donor countries share the burden of hosting refugees, this could be treated as part of their contribution to global welfare.

Variations in how countries applied these rules led to concerns about consistency and comparability of reporting. In response, the DAC established a Temporary Working Group on Refugees and Migration, which worked on clarifying how these costs should be recorded. In October 2017, members endorsed a set of five specific clarifications to the reporting directives to improve transparency and consistency. These clarifications were incorporated into DAC statistical reporting guidance, and DAC members were encouraged to align their methodologies accordingly.

Source: Carsten Staur, “The elephant in the room: In-donor refugee costs”, blog, 11 March 2023 (viewed on 16 December 2025)

3.38 In the absence of donor agreement on a more restrictive definition, the OECD-DAC recommended in 2017 that donors take “a conservative approach to reporting on this item”, so as “not to inflate ODA and to protect the integrity of the concept”.48 Following a 2022 review of donor reporting practices, the OECD-DAC reiterated its recommendation: “Members are encouraged to follow a conservative approach for counting in-donor refugee costs in ODA in line with the Clarifications, given the potential impact on development co-operation budgets.”49

3.39 The OECD-DAC Chair Carsten Staur stated in 2023 that: “The Secretariat has also encouraged DAC members to be conservative whenever they make their assessments – not to overreport, but to act on the side of caution.” He added that: “Even though these costs can be reported as ODA, this does not mean that a country must do so.”50

The UK has taken an expansive approach to reporting IDRC relative to many other donors, although this is generally within the scope of the international guidance

3.40 As the department responsible for the UK’s ODA reporting, FCDO liaises regularly with the OECD-DAC on the UK’s reporting practices, and supports and closely monitors reporting by the various UK departments responsible for IDRC. ICAI has previously found that, in general, the UK operates within the OECD-DAC reporting guidance.

Table 4: Comparison of the UK approach to that of other OECD-DAC members

| Issue | UK practice | Examples from other |

|---|---|---|

| Inclusion of in-donor refugee costs as part of ODA | The UK includes these costs | Australia and Luxembourg do not count any refugee or asylum support costs as ODA at all |

| Failed asylum claims | The UK includes support costs for asylum seekers whose claim is ultimately unsuccessful | Belgium does not include support costs for asylum seekers whose application for refugee status ultimately fails |

| Asylum seekers from safe countries | The UK reports all associated costs of people presenting asylum claims | Iceland does not include costs for asylum seekers arriving from ‘safe’ countries if almost all asylum applications from those countries are rejected |

| Health and education services | The UK includes an imputed share of health and education costs, based on number and age profile of refugees and asylum seekers | Spain does not include primary schooling as an in-donor refugee cost. Belgium only includes marginal costs such as textbooks and school supplies when counting ODA-eligible education costs. Slovenia only includes health services provided within asylum centres, and not use of national health services by asylum seekers |

| Administrative costs | The Home Office charged £75 million in administration and management costs to the ODA budget in 2023 | Austria, Greece, Iceland and the Netherlands do not report any administrative costs |

| Accommodation | The UK includes both emergency and dispersed accommodation costs incurred within the first 12 months | The Netherlands does not include social housing as ODA – only the temporary accommodation provided to recent arrivals. Sweden stopped reporting compensation to local authorities for refugee resettlement costs from 2020 onwards |

Source: Organisation for Economic Cooperation and Development Data Explorer, ‘DAC members’ methodologies for reporting in-donor refugee costs in ODA’, 7 May 2025 (viewed on 16 December 2025)

3.41 However, ICAI has also previously found that the UK has not adopted a conservative approach to calculating and reporting IDRC, as recommended by the OECD-DAC. ICAI concluded that: “The UK’s method of calculating in-donor refugee costs seems to be within the rules and is more transparent than that of many donors, but it cannot be said to follow a conservative approach.”51

3.42 In interviews with ICAI, FCDO officials have offered the view that the DAC recommendation on a “conservative approach” applies narrowly to the use of modelled or estimated costs, and not to the question of which items to report as IDRC. However, various OECD documents indicate that the guidance on a conservative approach is more general and is offered to protect the integrity of aid statistics (see the quotes in para 3.38 and 3.39). A 2023 government review of the UK’s methodology for reporting IDRC makes no mention of the need to be conservative, the government rejected explicitly the recommendation to follow a more conservative approach in ICAI’s 2023 rapid review, and the narrow interpretation was still offered during the preparation of this review. The result of the UK’s interpretation is that, while FCDO describes its modelling as conservative, the examples in Table 4 show that the UK is expansive in its inclusion of IDRC that are reported as ODA, in comparison to other DAC donors.

3.43 In interviews with ICAI, UK government officials have also stressed that the UK is simply following mandatory reporting rules. However, it is notable that other donors (such as those cited in Box 5) have taken steps to reduce the level of IDRC included in their ODA reporting, and that this is considered fully compliant with OECD-DAC reporting standards. In addition, the UK chose not to report IDRC until 2010, following their introduction into the 1988 international ODA definition. The UK’s approach is therefore a policy choice, rather than the application of a mandatory reporting requirement. This can be seen further in the OECD-DAC mid-term review of the UK, which suggests that: “implementing a cap on the amount of ODA that can be spent domestically…would help to prevent the negative impact of sudden increases in in-donor costs on programming in future”.52

Box 3: The UK’s continued use of ‘imputations’ for some costs risks over-reporting

OECD-DAC 2017 guidance on reporting IDRC specifies that donors can report “temporary sustenance” for refugees and asylum seekers (such as food and shelter) for 12 months after their arrival, but not the costs of long-term integration into the host country. This would include the cost of basic or emergency healthcare. However, the OECD-DAC has stated that: “Direct costs attributable to ODA-eligible services to refugees are reportable. Members should refrain from using imputations.” This means that donor countries should report the actual costs of temporary services provided to refugees and asylum seekers, rather than an assumed share of the cost of public services offered to the population at large. The DAC accepts that reporting of these costs may include estimates of “costs of a temporary nature provided through national systems”, provided that the donor is able to provide a clearly defined estimate of the number of refugees and asylum seekers benefiting from a particular service. The UK asserts that its approach reflects this provision.

The rationale for distinguishing estimates in limited circumstances from use of imputations more widely is that using imputations “implies that refugees benefit from the services available to all citizens, which raises the question of whether these costs have a permanent rather than temporary nature in which case they can be seen to promote integration of refugees and should be excluded from ODA.”53 The 2022 OECD-DAC report on donor compliance with IDRC reporting guidelines identified the UK as one of the DAC members still using imputations. It states: “In the United Kingdom, the Home Office reimburses local authorities for education and health costs: for education, the calculation is based on the number and age of refugees on arrival in the country; for health it is based on a unit cost calculated by using the asylum seeker age profile and applying a specific age-related per-head cost.”54 Canada uses a similar method. By contrast, Slovenia reports only the costs of health services provided within asylum centres, but not the costs of refugees or asylum seekers making use of health centres or public hospitals in the vicinity.

ICAI’s 2023 review of UK aid funding for refugees and subsequent follow-up noted that the UK’s continued use of modelling instead of reporting actual incurred costs carried risks of over-reporting, and that it was difficult to assess if estimated costs were “realistic and conservative”. We were not able to find evidence that this has changed.

3.44 The failure to adopt a conservative approach to IDRC reporting has resulted in the UK being an outlier among donor countries in its reporting practices. The UK makes extensive use of modelling and ‘imputations’ (attributing a share of the costs of general public services to refugees and asylum seekers), even though this is contrary to OECD-DAC recommendations (see Box 3). It also interprets certain costs in an expansive way. For example, it reports the full cost of private sector accommodation contracts, irrespective of the occupancy rates of the accommodation – effectively billing the cost of empty hotel rooms to the aid budget (see Box 4).

3.45 Reporting practices vary, and an overall lack of transparency make like-for-like comparison difficult, but ICAI’s benchmarking of UK reporting against two comparator countries (the Netherlands and Sweden) across 18 areas reveals that the UK takes the most expansive option in 12 categories (compared to ten and nine respectively) and the least expansive option in only two categories (compared to nine and six respectively). For example, the UK includes transport costs as ODA-eligible, while neither Sweden nor the Netherlands charge these against ODA. Table 4 above also compares the UK to other OECD-DAC members.

Box 4: Do empty hotel rooms count as support for asylum seekers and refugees?

Faced with insufficient accommodation to house growing numbers of refugees and asylum seekers, the Home Office established a series of contracts with private companies to rent hotels. The limited data available shows that, in December 2023, the Home Office had contracts covering around 400 hotels with around 64,000 beds, at a cost of £274 million. However, only 45,800 beds were actually occupied.55 Given that 64% of total Home Office expenditure on asylum seekers in that year was ODA-eligible (in other words, spent on arrivals in their first year), this implies that nearly £50 million in ODA went towards unoccupied hotel rooms in that December alone, or £600 million for the year.56

This was not necessarily in contravention of OECD-DAC rules, if the contracting of entire hotels was necessary to provide accommodation at the scale required. However, charging empty hotel rooms to the ODA budget cannot be considered a conservative approach to reporting IDRC, nor good value for money in the use of UK aid.

The UK’s expansive approach to reporting in-donor refugee costs has exacerbated the wider challenges to its budgetary management of development spending

3.46 In recent years, there has been a sharp rise in the share of international aid spent on IDRC, which increased more than 2.5 times from 2021 to 2022, reaching $31.8 billion (£23.5 billion) or 17.3% of global ODA.57 This rise has occurred across many donor countries, triggered by global forced displacement crises in Afghanistan, Ukraine and other places. However, it has had a disproportionately large impact on UK aid.

3.47 While it is not possible from public data to judge how far this is driven by an actual rise in costs, and how far by expansive reporting, the UK has chosen not to adopt any of the techniques used by other donor countries to minimise disruption to their remaining aid budgets – such as capping the reporting of IDRC. The government rejected ICAI recommendations from 2023 to introduce a cap on the amount of ODA allocated for IDRC and for more conservative methods for calculating IDRC. In the period from 2020 to 2024, nearly £9.97 billion (14.5%) in ODA has been diverted away from developing countries to spend on refugees and asylum seekers in the UK.58

3.48 This is in contrast not only to Sweden and the Netherlands, neither of which have allowed reporting of IDRC to reduce their overall support for developing countries, but also to G7 countries France and Germany, which have kept reporting of IDRC separate from programmes for development priorities overseas. This is in line with the OECD-DAC preference that “most donors report that donor refugee costs are additional to the rest of their ODA programmes”, unlike the approach taken by the UK.59

Box 5: Comparing the UK’s approach to rising in-donor refugee costs with Sweden and the Netherlands

Like the UK, both the Netherlands and Sweden have seen sharp rises in IDRC as a result of repeated increases in asylum seeker arrivals over the past decade. The recent history for each of these two comparator countries is summarised below, along with the measures they have taken to mitigate these increases. These examples show some of the options that the UK could have taken to mitigate the impact of rising IDRC on its aid budget.

Sweden is one of the most generous donor countries, having met the UN 0.7% target every year since 1974, and frequently spending more than 1% of its GNI on aid.60 At several points over the last 15 years, large refugee movements have led to spikes in Sweden’s ODA expenditure. In 2015, for example, total Swedish aid reached 1.4% of GNI following a surge in asylum seekers from Syria and elsewhere. Unlike the UK, Sweden did not set an ODA spending limit and therefore permitted its overall aid budget to accommodate the arrivals. However, the volatility of IDRC was nonetheless recognised as harmful to Swedish development cooperation, contributing to the fracturing of a longstanding political consensus in favour of aid. Sweden therefore established a fixed aid budget for the period from 2023 to 2026, while capping IDRC and other deductions from overseas spending at 8% of the total budget. Sweden also implemented measures to lower expenditure on IDRC, which for the time being remain below the 8% cap. These measures, such as offering temporary (rather than permanent) residence permits and introducing language and cultural values tests, have worked to disincentivise asylum applications. In 2024, asylum applications fell to under 10,000.

The Netherlands has also experienced sharp rises in IDRC. Like the UK, it has faced a severe shortage of accommodation. Given the high costs of emergency housing, its accommodation costs rose from £1.4 billion (€1.6 billion) in 2022 to £2.4 billion (€2.7 billion) in 2023, as a result of increases in both numbers and unit costs. The government agency responsible for the reception of asylum seekers has exceeded its budget in 21 of the last 23 years. In March 2024, the Council on International Affairs identified that: “the high level of unpredictability is problematic because it undermines the quality of the Netherlands’ spending on development co-operation”.61 In response to these pressures, the Dutch government has taken two major policy decisions. The first was to exclude all costs associated with hosting Ukrainians (apart from a one-off contribution of €150 million in 2021) from the ODA budget. It has also now decided to introduce an IDRC cap of 10% of ODA from 2027.