The changing global context for development cooperation

Foreword

The Independent Commission for Aid Impact (ICAI) published its report ‘How UK aid is spent’ in February 2025. At the start of a new Commission and following the formation of a new government, we wanted to understand recent trends in the global context for international development and clarify how much, where, and how UK aid was being spent. The report highlighted the trade offs and choices facing a new government in the use of official development assistance (ODA). It was also intended to provide a ‘baseline’, to which ICAI would return to at the end of the Fourth Commission, to assess progress.

Since that report was published, there have been profound shifts both in the global environment for international development and in the UK’s own approach to development cooperation. The year 2025 saw a contraction of ODA resources globally that was unprecedented in both scale and speed, including in the UK where ODA will be reduced from 0.5% to 0.3% of gross national income (GNI) by 2027. As a result of this, and amid wider geopolitical changes, the international development system is undergoing rapid contraction and repositioning. In this context, the UK has adopted a fundamentally different approach to development cooperation – not just in the amount it spends, but in where that money goes and how it is deployed.

This report was commissioned to update our analysis of the backdrop against which the UK is making consequential decisions about where to focus with a reduced budget and how to deliver impact. Individually and together, economic trends, shifts in the geopolitical context, and reduced levels of development finance available to the poorest countries are putting pressure on the international development architecture that the UK both influences and delivers through. These choices, and how they are implemented, will be critical in determining whether UK development cooperation continues to deliver meaningful impact and value for money in a context of rising need, constrained resources, and heightened risk.

In 2025, ICAI’s remit was broadened to cover not just all of the UK government’s ODA, but its development cooperation more broadly. In future reviews, ICAI will therefore examine how the UK uses its expertise and global influence, as well as its aid budget, to help tackle development challenges.

The analysis in this report will inform ICAI’s review work, and we hope that publishing it will contribute to the debate on the future of UK aid and development cooperation more broadly.

1. Introduction

The Independent Commission for Aid Impact works to improve the quality of UK development cooperation through robust, independent scrutiny. We provide assurance to the UK taxpayer of the effectiveness and value for money of UK development assistance.

This report provides an update on the changing global context for international development cooperation since ICAI’s previous How UK aid is spent report published in February 2025.

The first section surveys the opportunities and challenges facing developing countries, looking at progress towards the UN Development Agenda 2030, global economic conditions, trends in conflict, climate change and population displacement, and the increasingly challenging geopolitical context. It explores how complex interactions between global economic turbulence and political trends have combined to make the 2020s a particularly challenging decade for international development.

The second section looks at the seismic changes underway in the international development sector, including the closure of the US Agency for International Development (USAID) and the unprecedented reductions in official development assistance across major donors.1 The ODA reductions have in turn had major impacts on the multilateral systems for humanitarian response and development assistance. The report concludes by summarising some of the key challenges that the UK aid programme will need to consider as its approach to international development evolves.

This is a purely factual account, based on publicly available sources, capturing information available in early 2026. It is necessarily selective in its presentation of a complex picture.

2. The global development context

The 2020s risk becoming a ‘lost decade’ for global development

A global development emergency is unfolding

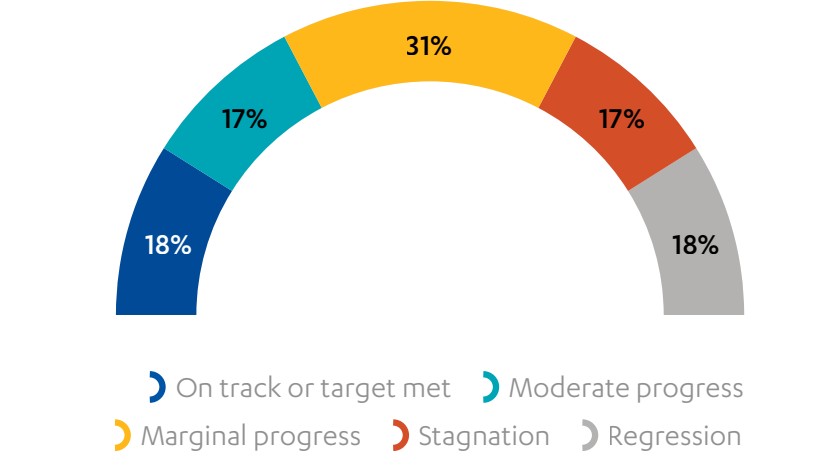

The COVID-19 pandemic, rising conflict, climate disruption and continuous global economic turmoil have all set back progress towards achieving the Sustainable Development Goals (SDGs) – the global development agenda agreed by all UN member states.2 According to the latest update, only one-third of 137 SDG targets are on track or making even moderate progress. Many have stagnated (17%) or gone backwards (18%) – a situation the UN describes as a ‘global development emergency’.3

Figure 1: Most UN targets show marginal progress, stagnation or regression

Semicircular chart showing progress against the UN Sustainable Development Goal (SDG) targets as of 2025. Most show marginal progress (31%), 18% are met or on track, while another 18% are regressing.

Source: United Nations Department of Economic and Social Affairs, ‘The Sustainable Development Goals report 2025’, July, 2025

The UN estimates that a financing gap of $4.3 trillion annually would need to be filled to achieve the SDGs by 2030.4 Development finance comes from a range of public and private sources, both domestic and international, including commercial lending, foreign direct investment, remittances and official development assistance (ODA). ODA represents only a minor share of the total, although it remains vital for low-income countries and those affected by conflict and fragility.5

Progress towards the SDGs is increasingly constrained

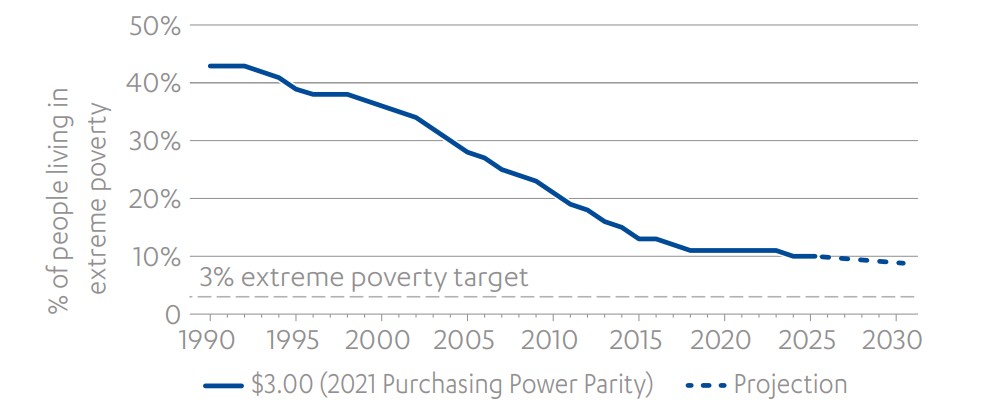

The SDGs commit the international community to “end poverty in all its forms, everywhere”. Only 20% of countries are on track to halve their national poverty rates by 2030. 6 After falling rapidly for two decades, the extreme poverty rate has stalled at around 10% (see Figure 2). Extreme poverty is increasingly concentrated in rural areas of sub-Saharan Africa and in conflict-affected and climate-vulnerable locations elsewhere.

The SDG era has delivered significant gains in access to basic services, but several goals are now off track.

- Hunger: Global hunger rose from 7.5% in 2019 to 9.1% in 2023. High food prices mean that an additional 383 million people face moderate or severe food insecurity.7

- Education: Access and completion rates have continued to improve across all levels of schooling. However, around 36% of school-aged children remain out of school, and slow gains in literacy and numeracy indicate weak progress on learning outcomes.8

- Gender equality: At the current rates of change, achieving the empowerment of women and girls and ending gender based violence and discrimination will take another century.9

- Water and sanitation: Progress has been too slow to meet the 2030 target, with 2.2 billion people still lacking safely managed drinking water and 3.4 billion lacking basic sanitation.10

These trends underline the importance of financing in shaping SDG outcomes. Improvements in access to services have largely been driven by investments made before recent shocks, while the stalling and reversal seen in hunger, health, and learning outcomes reflect the impact of tighter global financial conditions, high debt burdens, and declining aid flows.

Figure 2: Global extreme poverty has stagnated at around 10%

Line chart showing the global extreme poverty rate falling sharply from 43% in 1990 to around 10% by 2020, where it has stagnated. Projections to 2030 suggest only marginal further decline, remaining well above the 3% UN target.

Source: United Nations Department of Economic and Social Affairs, ‘The Sustainable Development Goals report 2025’, July 2025

Persistent global economic instability is undermining growth prospects

Instability and a retreat from globalisation are re-shaping trade and investment

From the early 2020s, a series of overlapping shocks – beginning with COVID-19 – have ushered in a lengthy period of economic instability. For developing countries, this has translated into weak growth, inflation and rising macroeconomic pressures. Disruption to the supply of essential commodities such as fuel and fertiliser has driven up prices, with knock-on effects for power generation, manufacturing and food production.11

Geopolitical fragmentation is causing long-term shifts in trade patterns, weakening the traditional globalisation-led growth model.12 Global value chains, once central to job creation, are under strain. Firms are re-shoring or re-regionalising production, while advances in automation are reducing demand for cheap labour.13

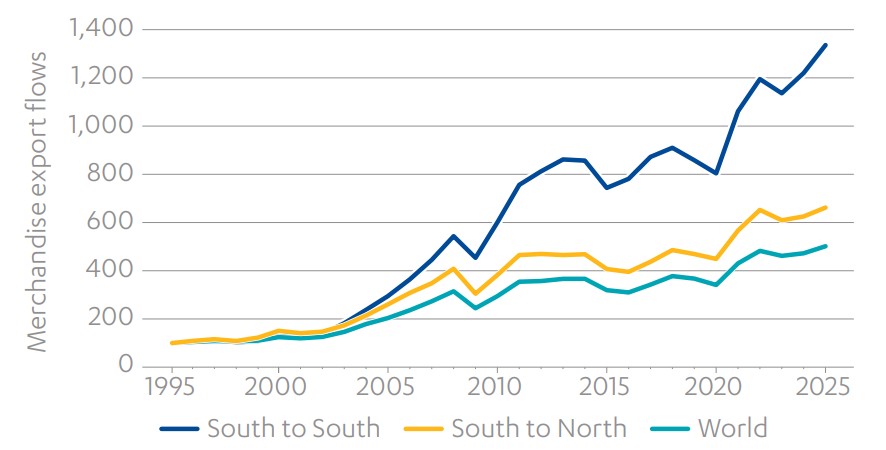

However, regional integration and South-South trade is growing rapidly, accounting for over a third of global trade and 57% of developing country exports.14 Mechanisms such as the African Continental Free Trade Area, which represents a potential market of over a billion people, could become a more important engine for growth than exports to OECD countries, although there are regulatory and infrastructure barriers to be overcome.15

Figure 3: Trade between developing countries is growing rapidly

Line chart showing trade flows from 1995 to 2025. Trade between Global South countries has grown the fastest, far outpacing both South-to-North trade and overall world trade growth.

Source: United Nations Conference on Trade and Development, ‘Global Trends Update (January 2025): Top Trends Redefining Global Trade in 2026’

Recent shifts in global investment patterns are disadvantaging low-income countries

Although foreign direct investment (FDI) has recovered in aggregate since the pandemic, investment flows to the poorest countries are flat or declining.16 In 2023, FDI inflows to low income countries, as a share of gross domestic product, were around half of where they stood before the global financial crisis.17 The rapid expansion of artificial intelligence (AI) is concentrating investment into capital-intensive activities in countries with strong skills bases and infrastructure, rather than into labour-intensive activities, weakening prospects for jobs and growth in many low-income settings.

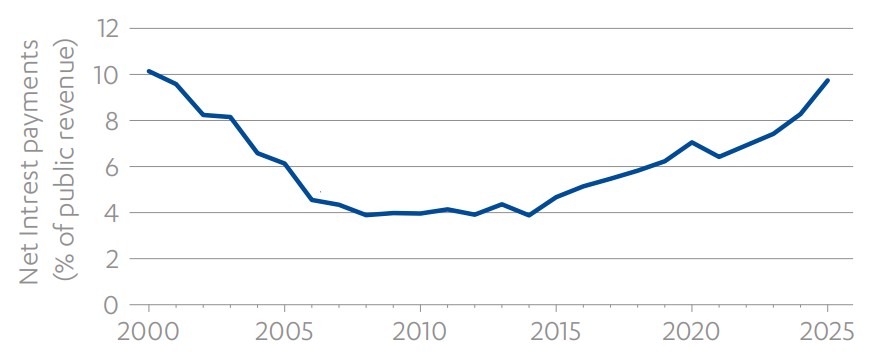

The debt burden is at a historic high and remains systemic

The debt crisis in developing countries eased slightly in 2025, with a small number of countries such as Ghana and Sri Lanka reaching deals with their creditors. However, overall debt levels remain at historic highs, and net debt flows have been negative since 2022, meaning that developing countries are paying back more in external debt service than they receive in new lending.

International policy forums including the G20 and the 2025 International Conference on Financing for Development in Seville have called for reform to global debt resolution frameworks. In parallel, some African countries have proposed the creation of a ‘borrowers club,’ to strengthen collective action and rebalance negotiating power with creditors.

Figure 4: How much on average developing countries spend on servicing debt

Line chart showing developing countries’ median average spend on net interest payments from 2000 to 2025, as a percentage of public revenue. After falling from around 10% in 2000 to a low of around 4% between 2008 and 2014, the rate has risen back to 9.5% by 2025.

Source: United Nations Development Programme, ‘UNDP Debt Update: Development gives ways to debt’, 25 February 2025

Climate change and development outcomes remain closely linked

Climate change is accelerating across multiple dimensions

Global climate change continues to accelerate alarmingly. The years from 2015 to 2025 were the 11 warmest in 176 years of records.18 Greenhouse gas emissions in 2024 were the highest ever recorded, up 1.3% from 2023.19 This is already having dramatic consequences for developing countries, in the form of weather-related disasters, declining food security, large-scale population displacement and wider economic losses.

Global mitigation commitments are insufficient and in some cases backsliding

International action remains well short of what is needed to reverse these trends. There has been backsliding on key pledges, including on phasing out fossil fuels and halting deforestation. Of 45 indicators of progress towards the Paris Agreement goal of holding global temperature rise to within 1.5oC of pre-industrial levels, none are on track.20 It is estimated that, for every dollar spent on protecting nature, $30 are invested in activities that destroy it.21 However, the deployment of renewable energy continues at pace, and in 2025 renewables overtook coal as the largest source of electricity generation.22

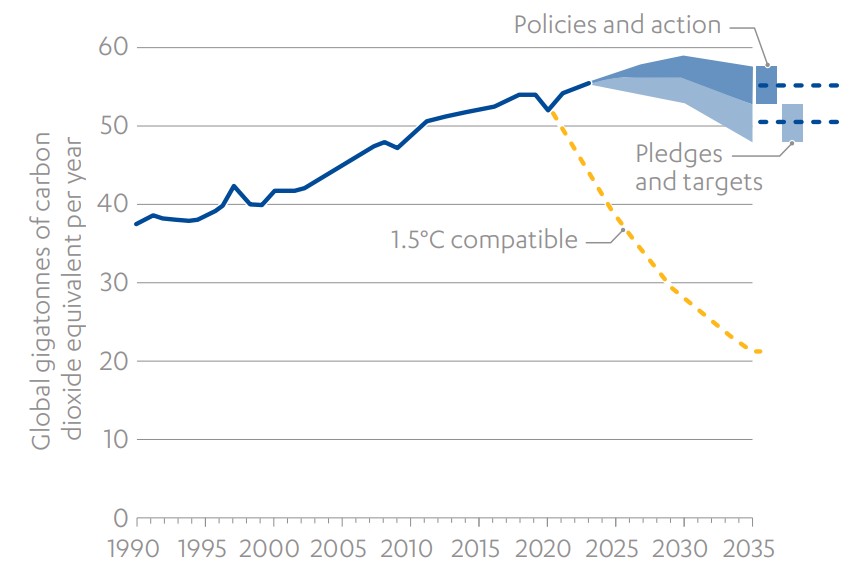

As Figure 5 shows, current national climate policies and commitments collectively fall well short of the 1.5oC pathway. Even if fully implemented, they would leave a 26-31 gigatonne emissions gap, leading to median global warming of 2.8°C by 2100.23 In practice, these commitments are often conditional on external finance.

New climate finance goals have been agreed, but fall well short of need

In 2023, total climate finance (including domestic investments) reached $1.9 trillion, compared to the estimated $6.3 trillion needed to avert the worst impacts of climate change.24 International climate finance (ICF) for developing countries from bilateral donors is falling, and is increasingly loan-based, which makes it less suitable for poorer countries. There are serious shortages of funding for adaptation, and for fragile states in particular, which are acutely climate-vulnerable but receive only 10% of ICF.25

The Fund for Responding to Loss and Damage, which was established to compensate developing countries for climate change-related losses, has received $921 million in pledges and begun its operations. However, with projected loss and damage from climate change of up to $580 billion by 2030, there are questions about its significance.26

The COP29 climate conference in 2024 agreed a New Collective Quantified Goal of at least $300 billion in ICF for developing countries by 2035. Although triple the previous target, it remains far short of need, and was denounced by the Least Developed Countries Group as “a staggering betrayal of the world’s most vulnerable”. Critics say it also lacks precise definitions and robust enforcement.27

Figure 5: Greenhouse gas emissions since 1990 and future projections

Line chart showing global emissions rising steadily, reaching around 54 gigatonnes of carbon dioxide equivalent per year by 2024. Current projections show emissions remaining between 48 and 57 gigatonnes, well above the roughly 20 gigatonnes needed to meet the 1.5°C Paris Agreement target.

Source: Climate Action Tracker, November 2025

Armed conflict has grown in scale and intensity and the human cost is rising

Armed conflict is at its highest level since the Second World War, and rising

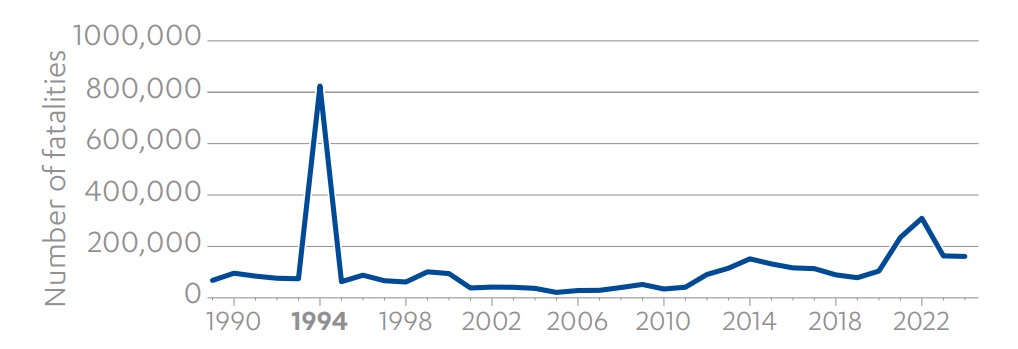

Over the past 15 years, global conflict has risen in scale and intensity, and become more lethal. The number of state-based conflicts recorded in 2024 was the highest since 1946.28 Fatalities from conflict have surged in the past five years as a result of major wars in Ukraine, Sudan and the Middle East.29 Children are disproportionately affected by conflict, with 12,000 killed or maimed (the highest since UN records began 30 years ago)30 and 48.8 million displaced by conflict in 2024.31 Attacks on schools in conflict zones have increased by 44% over the past year.32

Figure 6: Global fatalities from organised violence between 1989 and 2024

Line chart showing a sharp peak of around 820,000 fatalities in 1994, reflecting the Rwandan genocide. Fatalities have risen sharply since 2020, reaching around 310,000 in 2022 before declining to around 160,000 in 2024.

Source: Shawn Davies, Therése Pettersson, Margareta Sollenberg and Magnus Öberg, ‘Organized violence 1989-2024, and the challenges of identifying civilian victims’, 2025

Conflict is becoming more lethal, less constrained by law and increasingly shaped by new technology

There has been a marked decline in respect for international humanitarian law, reflected in frequent attacks on civilians with civilian casualties rising by 31% per year since 2010 and more attacks on humanitarian workers and health facilities.33 At the same time, there is increasing concern that the muted international response to violations of international law in recent conflicts is contributing to a long-term erosion of international norms.34

Advances such as AI-assisted targeting and autonomous weapons systems are altering how conflict is conducted. Widespread availability of inexpensive commercial technologies has meant that armed non-state groups have access to inexpensive commercial drones, which can be adapted to cause harm.35 This has increased the reach and lethality of non-state violence.

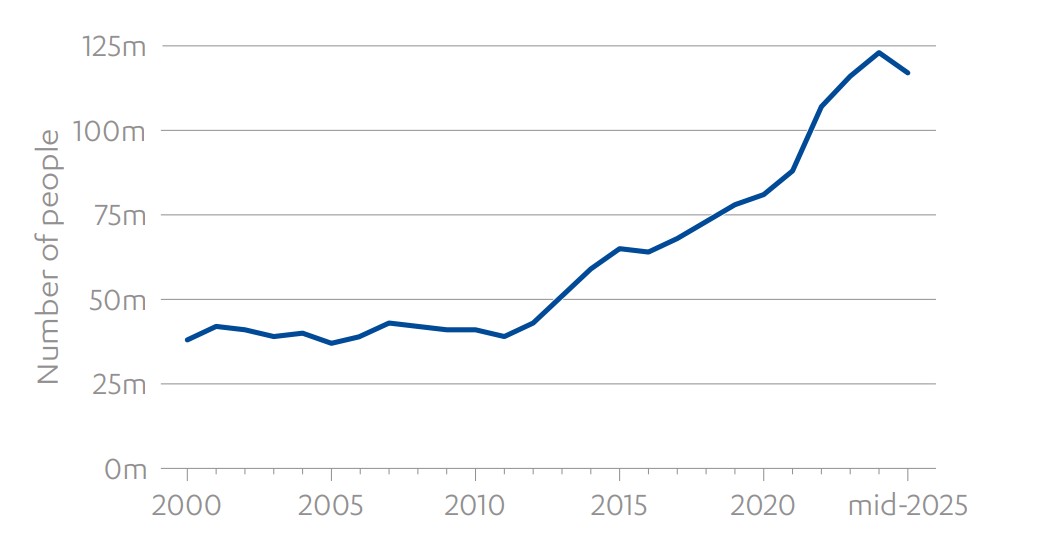

Displacement is widespread, persistent and increasingly complex

Around the world, 117.3 million people are forcibly displaced, the majority of whom are displaced within their own country. The total has doubled over the past decade (see Figure 7), due mainly to conflict and violence. This includes approximately 50 million refugees worldwide, with 71% being hosted in developing countries36 and 66% having been displaced from their home country for more than five years.37

2025 also saw an increase in the numbers of refugees returning to their home country. More than three million Syrian refugees returned home voluntarily after the fall of the Assad regime in December 2024,38 while 2.8 million Afghans were compelled to return, mainly from Iran and Pakistan.39 These contrasting movements highlight the persistence of displacement and the different conditions shaping return.

Figure 7: Forced displacement over the past 25 years

Line chart showing the number of people forcibly displaced worldwide from 2000 to mid-2025. Numbers remained relatively stable at around 40 million until 2012, before rising to a peak of around 120 million by 2024 before falling slightly.

Source: United Nations High Commissioner for Refugees, ‘Mid-Year Trends 2025’, 4 November 2025 (viewed on 21 March 2026)

Democratic regression, threats to human rights and closing civic space shape prospects for development

Democratic decline is deepening

In 2025, 60 countries experienced declining political rights and civil liberties, with only 34 registering improvements.40 For the first time in 20 years, the world has fewer democracies than autocracies. Just 20% of the global population live in countries rated as fully ‘free’ – down from 46% two decades ago.41 Disaffection with democratic governance is increasingly evident and widespread, including in OECD countries.42

The drivers of democratic regression are multiple and mutually reinforcing, including declining electoral integrity, oligarchic capture of state institutions, widening economic inequality, stagnation and precarity, digital disinformation and polarisation.43

At the same time, external support for democracy has weakened across multiple fronts. Public funding for development assistance to strengthen democratic governance has reduced, especially from the US, which was historically the largest funder of this area of activity. The closure of USAID in 2025, and the termination of more than 1,600 democracy-related grants affecting organisations in 120 countries, represented a serious rupture in development assistance to governance and civil society.44 In parallel, there has been a marked increase in financial support from private sources for anti-rights groups and illiberal political movements.45

Human rights and civil liberties are being eroded

The rule of law has weakened in a sizeable majority of countries over the past eight years, with 68% registering declines and only 32% improving.46 There is a global rise in media censorship, election interference, limitations on judicial independence and restrictions on civic space.47 According to the UN, a quarter of countries report a backlash against women’s rights, including declining legal protection and reduced support for women’s organisations.48 Forty-one of the most fragile countries lack even minimal protection of citizens from wartime violence, insurgencies, crime and unaccountable security forces.49

Rapid technological change is proving a double-edged sword for human rights

Around the world, complex new policy and regulatory challenges are being posed by rapid technological development.

The rise of online spaces and new technologies, including AI, are creating complex new human rights risks in different ways:

- Surveillance and privacy erosion, including mass data collection by governments on activists, dissidents, journalists and minorities, facial recognition and hacking software.

- Censorship and disinformation, including internet shutdowns during protests, algorithmic amplification of hate speech and AI-generated deepfakes.

- Bias and discrimination, driven by the use of AI and algorithmic decision-making in public services, banking, hiring and policing.50

New technology and tools can also be used by citizens and movements to open new forms of civic space, amplify voices and provide new avenues to hold power accountable. A recent example has been the rise of Gen Z protests driven by social media, which featured in 11 countries in 2025,51 reflecting concerns such as corruption and high youth unemployment. While online organisation can lead to rapid mobilisation of protest, further conditions, such as stable leadership and institutional structures, may be required for durable democratic movements.

A sharp contraction in budgets is reshaping the role of ODA

Significant reduction in ODA by major donors in 2025 was an unprecedented shock to the global aid system

2025 brought seismic changes in the global development sector. Over the course of the year, 11 major donors – together accounting for three-quarters of global aid – announced ODA reductions.52

In February 2025, the UK government announced the aid target would be reduced from 0.5 to 0.3% of national income by 2027 to fund increased defence spending. The closure of USAID in July 2025 and the cancellation of 80% of its programmes translated into a $35 billion (48%) reduction in US ODA.53 In February 2026, Congress approved a new aid package of $50 billion, restoring US support in key sectors such as humanitarian aid and global health. However, the net effect remains a substantial reduction, with overall support 16% below the 2024 level.54

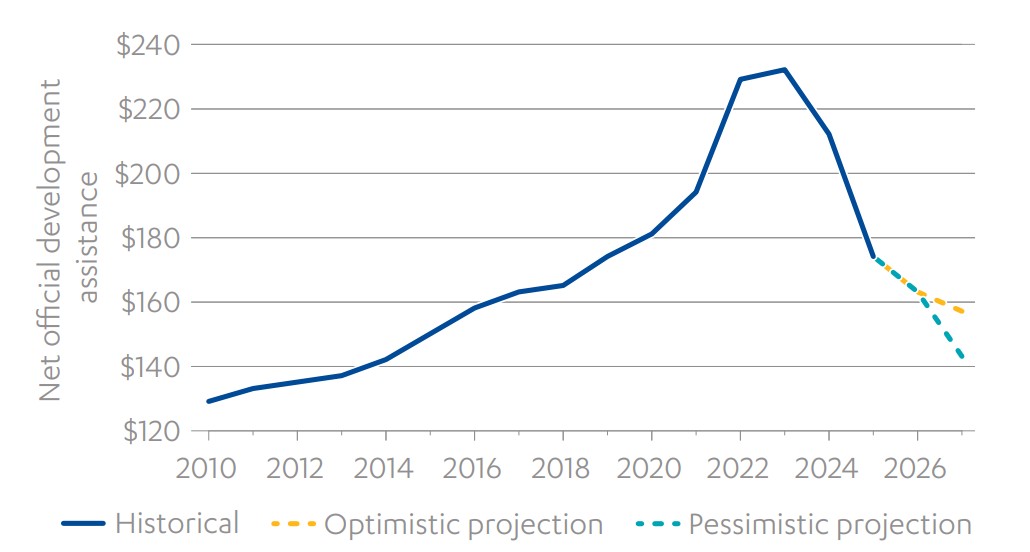

Globally, ODA fell by 23.1% – or $50 billion – in 2025 to $174.3 billion. The OECD projects further falls of 5.8% in 2026, to $164 billion, and by 10-18% in subsequent years. As Figure 8 shows, this suggests that global ODA may fall back to the levels seen in the 2010-2015 period. OECD analysis suggests that low-income countries and sub-Saharan Africa will be most affected.

Figure 8: Global aid looks likely to fall back to 2010-15 levels

Line chart showing net official development assistance (ODA) from 2010-27. After rising to a peak of $230 billion in 2023, ODA has fallen sharply, with projections suggesting a further decline to between $145 and $160 billion.

Source: OECD DAC Statistics & Preliminary 2025 ODA data

Attention has turned towards alternative ways of filling the gap in development finance

Falling ODA levels are also prompting donors to rethink how development is financed. The focus of the 2025 International Conference on Financing for Development in Seville put less emphasis on increasing the volume of grant aid, and more on addressing structural and systemic factors shaping development finance, including affordable borrowing, debt restructuring, domestic resource mobilisation, private investment, combatting illicit financial flows, and reform of the global financial architecture.55

Alongside global shifts, bilateral donors (including the UK) are increasingly aligning aid with foreign policy, security interests, trade, and migration objectives.

Donors are increasingly using scarce ODA to ‘leverage’ private capital

Donors are moving towards using limited ODA to mobilise private finance, reflecting the scale of investment needed to meet development and climate goals. Using ODA to absorb some risks faced by investors, instruments such as loan guarantees aim to increase private lending at affordable rates and to catalyse investment at scale.

OECD figures, however, suggest that results have been mixed. While the volume of private investment mobilised has increased, the majority of funds (around 88%) have flowed to middle income countries, where viable investment opportunities are more readily available. Many development finance institutions also report leverage ratios below 1:1, with each dollar of ODA mobilising around $0.20–0.30 in private finance.56

This has led to debate about the extent to which these approaches can fill financing gaps in the poorest and most fragile countries, although ambition to do so exists.57

3. The international development sector

The global humanitarian system is in crisis

Humanitarian assistance is no longer keeping pace with escalating need

Over the 2010s, humanitarian aid increased broadly in line with rising needs, peaking at $43.3 billion in 2022 following Russia’s full-scale invasion of Ukraine.58 Since then, however, funding has fallen rapidly. Between 2022 and 2024, total humanitarian funding declined by 15%, before dropping sharply by a further 55% in 2025. This is a cumulative reduction of $22.8 billion in three years.59

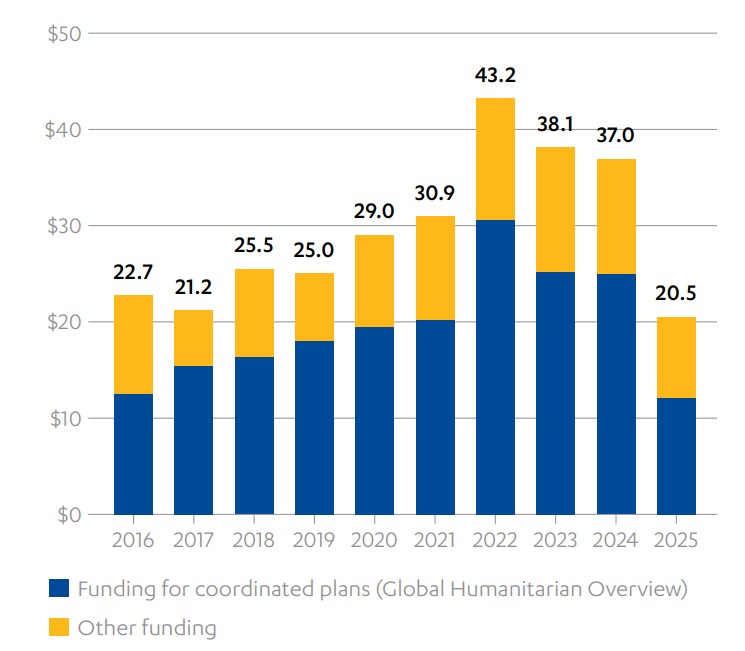

This contraction has happened at a time when humanitarian needs are at historic highs. Famine conditions have been declared in Gaza and Sudan, along with catastrophic levels of food insecurity in DR Congo, Haiti, Myanmar, South Sudan and Yemen.60

The humanitarian system is contracting, limiting coverage to the most acute, life-saving interventions

In response, the humanitarian system has been forced into ‘hyper-prioritisation’, limiting support to core life-saving activities in the most pressing crises. In 2025, 300 million people were assessed as in need of assistance, but only 88.2 million were covered by the UN Global Appeal and, even then, funding fell short by $3 billion.61

Figure 9: Global humanitarian funding between 2016-25

Stacked bar chart showing global humanitarian funding from 2016 to 2025, split between funding for coordinated plans and other funding. Total funding peaked at $43.2 billion in 2022 before falling to $20.5 billion in 2025, the lowest level in the period shown.

Core humanitarian principles are under threat

The international humanitarian system faces further severe challenges. 2024 was the deadliest year on record for humanitarian workers, with 383 fatalities, while humanitarian access in crises such as Gaza and Sudan has been heavily restricted.62

Experts have raised concerns about recent trends in humanitarian assistance provision, including the use of private contractors outside of UN coordination mechanisms, increased use of the military to deliver aid, and greater alignment with security and political objectives. Critics argue that these approaches put pressure on the principles of neutrality, impartiality and independence which underpin the international humanitarian system.63

The crisis is an opportunity for progress on localisation

Some commentators have suggested that the collapse in humanitarian funding would give impetus to localisation. Shifting funding, decision-making and leadership to more cost-effective local actors has been a longstanding but poorly operationalised reform commitment.64 While discussions on reform of the humanitarian system are ongoing, there is little evidence yet of meaningful shifts in funding. In the short term, budget reductions have led to reduced funding for local partners and narrowed the scope for meaningful partnership.65

The multilateral system faces urgent calls for reform and renewal

Multilateralism is under immense pressure

The multilateral system, still largely anchored in institutions designed after the Second World War, is facing growing challenges of effectiveness, legitimacy and inclusiveness. This is reflected in decision making gridlock, representation gaps, and a lack of action on pressing global challenges.66 Norms underpinning the UN Charter – including commitments to universal human rights and the rule of law – are being challenged more explicitly.67 Major conflicts involving permanent members of the Security Council expose the limits of the international peace and security architecture, particularly the constraints imposed by veto power.

At the same time, emerging powers and many countries across the Global South are pressing for greater voice and influence within multilateral institutions, highlighting a widening mismatch between global power realities and existing governance arrangements.68

Comprehensive multilateral reform is challenging to achieve in the short term

In the current geopolitical context, divisions and fragmentation make agreement on major multilateral reform difficult to achieve. Yet discussions on new forms of global cooperation continue in specific areas, including pandemic preparedness, international tax cooperation and climate action.

There has been an increase in intergovernmental ‘clubs’ and informal governance arrangements, such as the G7 and the G20, the BRICS group and transnational networks, such as the C40 coalition of cities committed to climate action. These new forums can enable coordination, however they operate alongside formal multilateral institutions. The growth of alternative arrangements suggests unmet demand for global governance at a time when comprehensive reform of the multilateral system seems out of reach.

Box 1: The UN80 process: a system-wide reform initiative

Launched by UN Secretary-General António Guterres in March 2025 to mark the UN’s 80th anniversary, the UN80 Initiative is a system-wide reform effort to enhance efficiency, agility, and impact amid shrinking resources.69 It is considering measures such as reducing the UN’s global footprint, merging agencies, and shifting to shared service and technology platforms. Although far-reaching, UN80 is limited to reforms that are within the authority of the UN Secretariat. Any fundamental changes would require agreement by UN Member States, through the General Assembly.

The UN faces a system-wide funding crisis

A survey of 31 multilateral organisations showed most facing budget reductions of 11-30% in 2025 and 2026, with a highly uncertain medium-term funding outlook.70 This crisis offers an opportunity for reform. The UN80 reform process is attempting to do this (see Box 1). However, it is struggling against a default tendency for funding cuts to intensify fragmentation and competition among agencies for shrinking resources.71

Pressures extend well beyond the UN to the wider international system. For example, the global trade regime is strained by unilateral trade restrictions and intensifying geoeconomic fragmentation, which have weakened rules-based cooperation.72 Rapid technological change – in areas including AI, cryptocurrency and automated weapon systems – is outpacing the development of effective international governance and regulatory frameworks.73

These trends highlight a widening gap between global challenges and the capacity of existing multilateral institutions to respond.

4. Conclusion

This report provides an updated outlook of the complex context for international development in which the UK has reduced ODA to 0.3% of GNI and announced its intention to modernise its approach to international development through four shifts: moving from donor to investor, from service delivery to systems support, from providing grants to lending expertise, and from prioritising international intervention to local leadership.

The government has identified a more focused set of priorities for the years ahead, including humanitarian response, global health, climate and nature, women and girls, and engagement in fragile and conflict affected states. Within a significantly constrained budget, spending plans rely on greater use of multilateral channels, shifting away from broad bilateral grant programmes in favour of system level interventions, expertise, and development finance instruments to achieve impact.

The government has restated its commitment to restore development spending to 0.7% of GNI as soon as fiscal circumstances allow.74 However, the allocations announced in March 2026 are consistent with operating at 0.3% in the near term. As the government fully implements its new approach, ICAI will continue to scrutinise these and other issues in the remaining years of the Fourth Commission:

- What outcomes will the UK prioritise in its international development cooperation? If ODA is increasingly framed as a strategic tool for leveraging additional resources, what outcomes is it expected to deliver, and how will success be defined and measured? How will the government maintain a clear focus on poverty reduction while further integrating development cooperation with foreign policy, security, trade, and migration objectives? Who is expected to benefit from this approach, and in which contexts? Given that extreme poverty, climate vulnerability, and conflict are increasingly concentrated in fragile settings, how will the UK balance investment in immediate humanitarian responses with longer term resilience and prevention in these contexts?

- How will the UK deliver effective development impact under the shift from donor to investor? Given the mixed evidence, how will the UK ensure that leverage-based approaches deliver impact on a meaningful scale? How will it demonstrate that mobilised finance is genuinely additional, and that such approaches reach low income and fragile countries? Will the UK continue to invest in governance and rights?

- How will the UK deliver development outcomes effectively and demonstrate value for money in an era of constrained resources and rising global need? How will results be defined, what kinds of partnerships will be prioritised, and how will the UK maintain credibility as a development partner with reduced spending? Will increased reliance on multilateral channels and system level interventions deliver better value for money than bilateral grant programmes? Can localisation be credibly advanced while funding is falling?

References

- 1 Organisation for Economic Co-operation and Development, ‘A historic decline in foreign aid: Preliminary 2025 ODA data’, data explainer, 9 April 2026 (viewed on 20 April 2026) ↩

- 2 Sustainable Development Solutions Network, ‘World at Risk of Losing a Decade of Progress on the UN Sustainable Development Goals’, June 2023 (viewed on 20 April 2026) ↩

- 3 United Nations, ‘The Sustainable Development Goals Report’, 2025, page 2 (viewed on 20 April 2026) ↩

- 4 United Nations Trade and Development, ‘SDG Investment Trends Monitor’, September 2023, page 4 (viewed on 20 April 2026) ↩

- 5 Organisation for Economic Co-Operation and Development, ‘States of Fragility 2022’, September 2022, page 6 (viewed on 27 April 2026) ↩

- 6 United Nations, ‘The Sustainable Development Goals Report’, 2025, page 8 (viewed on 20 April 2026) ↩

- 7 World Economic Forum, ‘Five years to go: Are we on track to meet the Sustainable Development Goals’, September 2025 (viewed on 20 April 2026) ↩

- 8 United Nations, ‘The Sustainable Development Goals Report’, 2025, page 16 (viewed on 20 April 2026) ↩

- 9 United Nations Development Programme, ‘The landscape of development: UNDP trends update 2026’, February 2026, page 8 (viewed on 20 April 2026) ↩

- 10 United Nations, ‘The Sustainable Development Goals Report’, 2025, page 20 (viewed on 20 April 2026) ↩

- 11 Deloitte Global Economics Research Center, ‘The Middle East conflict begins to cast a shadow on the global economy’, March 2026 (viewed on 19 March 2026) ↩

- 12 World Economic Forum, ‘Global Value Chains Outlook 2026: Orchestrating Corporate and National Agility’, January 2026, page 3 (viewed on 29 April 2026) ↩

- 13 McKinsey & Company, ‘A new trade paradigm: How shifts in trade corridors could affect business’, June 2025, (viewed on 19 March 2026) ↩

- 14 United Nations Conference on Trade and Development, ‘Global Trade Update (January 2026): Top Trends Redefining Global Trade in 2026’, (viewed on 21 March 2026) ↩

- 15 Atlantic Council, ‘Middle powers’ game-changing rivalries’, December 2025 (viewed on 21 March 2026); African Union, ‘African Integration Report 2025’, June 2025 (viewed on 18 March 2026) ↩

- 16 United Nations Conference on Trade and Development, ‘Global Investment Trends Monitor’, April 2025 (viewed on 21 March 2026) ↩

- 17 World Bank, ‘Foreign direct investment in retreat: Policies to turn the tide’, 2025, page 7 (viewed on 20 April 2026) ↩

- 18 World Meteorological Organization, ‘State of the Climate Update for COP30’, 2025, page 7 (viewed on 17 March 2026) ↩

- 19 Clea Shumer and others, ‘State of Climate Action 2025’, Climate Analytics, ClimateWorks Foundation, the Climate High-Level Champions, and World Resources Institute, page 9 (viewed on 20 March 2026) ↩

- 20 World Economic Forum, ‘The Global Risks Report 2025 20th Edition: Insight Report’, 2025, page 7 (viewed on 20 March 2026) ↩

- 21 United Nations Environment Programme, ‘Nature in the red: powering the trillion dollar nature transition economy – State of Finance for Nature 2026’, 2026 (viewed on 20 March 2026) ↩

- 22 EMBER, ‘Global Electricity Review 2026’, April 2026 (viewed on 29 April 2026) ↩

- 23 International Energy Agency, ‘Electricity 2026’, 2026, page 45 (viewed on 20 March 2026) ↩

- 24 Natalia Alayza and Gaia Larsen, ‘How to Reach $300 Billion – and the Full $1.3 Trillion – Under the New Climate Finance Goal’, World Resources Institute, 5 November 2025 (viewed on 12 March 2026) ↩

- 25 Manisha Gulati, ‘Course correcting climate finance: why current readiness models are failing fragile states’, ODI, 5 November 2025 (viewed on 16 March 2026) ↩

- 26 Preety Bhandari, Nate Warszawski, Deirdre Cogan and Rhys Gerholdt, ‘What Is ‘Loss and Damage’ from Climate Change? 8 Key Questions, Answered’, World Resources Institute, 5 May 2025 (viewed on 20 March 2026) ↩

- 27 LDC Group, ‘COP29: ‘A Staggering Betrayal of the World’s Most Vulnerable’, 24 November 2024 (viewed on 20 March 2026) ↩

- 28 Uppsala Conflict Data Program, ‘Uppsala Conflict Data Program – Department of Peace and Conflict Research’, March 2026 (viewed on 7 March 2026) ↩

- 29 Journal of Peace Research 62 (4), ‘Organized violence 1989-2024, and the challenges of identifying civilian victims’, Shawn Davies, Therése Pettersson, Margareta Sollenberg and Magnus Öberg, July 2025 (viewed on 21 March 2026) ↩

- 30 UN Secretary-General, ‘Annual Report on Children and Armed Conflict (A/79/878-S/2025/247)’, June 2025, page 3 (viewed on 22 April 2026) ↩

- 31 UNICEF, ‘Displacement Data’, June 2025 (viewed on 22 April 2026) ↩

- 32 UN News, ‘Attacks on schools surge by ‘staggering’ 44 per cent over the past year’, September 2025, (viewed on 22 April 2026) ↩

- 33 Journal of Peace Research 62 (4), ‘Organized violence 1989-2024, and the challenges of identifying civilian victims’, Shawn Davies, Therése Pettersson, Margareta Sollenberg and Magnus Öberg, July 2025, page 1224 (viewed on 21 March 2026) ↩

- 34 International Committee of the Red Cross, ‘ICRC Humanitarian Outlook 2026: A world succumbing to war’, December 2025, pages 1-2 (viewed on 12 March 2026) ↩

- 35 ACLED, ‘What’s driving conflict today? A review of global trends’, December 2025 (viewed on 19 March 2026) ↩

- 36 United Nations High Commissioner for Refugees, ‘Mid-year trends 2025’, November 2025, page 2 (viewed on 7 March 2026) ↩

- 37 United Nations High Commissioner for Refugees, ‘Global trends; forced displacement in 2023’, 2024 (viewed on 22 April 2026) ↩

- 38 United Nations High Commissioner for Refugees, ‘Historic return of displaced Syrians presents opportunity and urgent challenges’, December 2025, (viewed on 22 April 2026) ↩

- 39 United Nations High Commissioner for Refugees, ‘Afghanistan Situation: Afghan Returns Emergency Update #17’, December 2025, page 1, (viewed on 22 April 2026) ↩

- 40 Freedom House, ‘Freedom in the world 2025’, February 2025, page 12 (viewed on 8 March 2026) ↩

- 41 Freedom House, ‘Freedom in the world 2025’, February 2025, page 12 (viewed on 8 March 2026) ↩

- 42 Economist Intelligence Unit, ‘Democracy Index: What’s wrong with representative democracy?’, 2025, page 5 (viewed on 19 March 2026) ↩

- 43 Economist Intelligence Unit, ‘Democracy Index: What’s wrong with representative democracy?’, 2025, page 32 (viewed on 19 March 2026) ↩

- 44 International IDEA, ‘When Aid Fades: Impact and Pathways for the Global Democracy Ecosystem’, December 2025 (viewed on 23 April 2026) ↩

- 45 European Parliamentary Forum for Sexual & Reproductive Rights, ‘The Next Wave: How Religious Extremism Is Regaining Power’, April 2026 (viewed on 23 April 2026) ↩

- 46 World Justice Project, ‘Rule of Law Index 2025’, 2025, page 26 (viewed on 8 March 2026) ↩

- 47 V-Dem Institute, ‘Democracy Report 2025 – 25 years of Autocratization – Democracy Trumped?’, March 2025, page 6 (viewed on 8 March 2026) ↩

- 48 UN Women, ‘Women’s Rights in Review 30 years after Beijing’, March 2025, page 6 (viewed on 20 March 2026) ↩

- 49 Freedom House, ‘Freedom in the world 2025’, February 2025, page 19 (viewed on 8 March 2026) ↩

- 50 Amnesty International, ‘Technology’ (viewed on 20 March 2026); Human Rights Watch, ‘Technology and rights’ (viewed on 20 March 2026); Team Community, ‘What Are Digital Rights? And How Do They Impact You?’ (viewed on 20 March 2026) ↩

- 51 Erica Chenoweth and Matthew Cebul, ‘Why Gen-Z is rising’, Journal for Democracy 37(1), January 2026 (viewed on 19 March 2026) ↩

- 52 Organisation for Economic Co-operation and Development, ‘Cuts in official development assistance: OECD projections for 2025 and the near term’, June 2025, page 2 (viewed on 19 March 2026) ↩

- 53 Organisation for Economic Co-operation and Development, ‘Cuts in official development assistance: OECD projections for 2025 and the near term’, June 2025, page 3 (viewed on 19 March 2026) ↩

- 54 Department of State, ‘Foreign Operations and Related Programs, Congressional Budget Justification’, 2026, page 8 (viewed on 30 March 2026) ↩

- 55 International Peace Institute, ‘The Financing for Development Agenda after Sevilla: Aligning Commitments and Actions’, October 2025, page 2 (viewed on 30 March 2026) ↩

- 56 Andrew Apampa, ‘How much does a dollar of concessional capital mobilize?’, February 2023 (viewed on 30 March 2026); Charles Kenny, ‘Billions to Trillions is (Still) Dead, What next?’, April 2022 (viewed on 30 March 2026) ↩

- 57 International Monetary Fund, ‘Private Finance for Development: Wishful Thinking or Thinking Out of the Box?’, May 2021 (viewed on 19 March 2026) ↩

- 58 United Nations Office for the Coordination of Humanitarian Affairs, ‘Global Humanitarian Overview 2026’, December 2025, page 2 (viewed on 6 March 2026) ↩

- 59 United Nations Office for the Coordination of Humanitarian Affairs, ‘Global Humanitarian Overview 2026’, December 2025, page 2 (viewed on 6 March 2026) ↩

- 60 Global Network Against Food Crises, ‘Global Report on Food Crises 2025’, 2025 (viewed on 8 March 2026) ↩

- 61 United Nations Office for the Coordination of Humanitarian Affairs, ‘Global Humanitarian Overview 2026’, December 2025, page 2 (viewed on 6 March 2026) ↩

- 62 Humanitarian Outcomes, ‘Aid Worker Security report 2025’, August 2025, page 1 (viewed on 19 March 2026) ↩

- 63 Michael VanRooyen, ‘The Future of Humanitarian Aid: Navigating a Politicized and Fragmented Landscape’, Harvard Humanitarian Initiative, June 2025 (viewed on 23 April 2026) ↩

- 64 Tafadzwa Munyaka, ‘Funding Cuts by Traditional Donors and the Future of Localization: Power, Paradox, and the Politics of Aid’, CRU, July 2025 (viewed on 27 April 2026) ↩

- 65 MOPAN, ‘Multilateral effectiveness in a shifting landscape: mapping of multilateral organisations’ response to the current funding environment’, 2025, page 9 (viewed on 23 April 2026) ↩

- 66 High-Level Advisory Board on Effective Multilateralism, ‘A Breakthrough for People and Planet: Effective and Inclusive Global Governance for Today and the Future’, 2023 (viewed on 23 April 2026) ↩

- 67 UN Secretary-General António Guterres, ‘Secretary-General’s remarks to the Security Council – on Reaffirming the International Rule of Law’, 26 January 2026 (viewed on 23 April 2026) ↩

- 68 Norwegian Institute of International Affairs, ‘Emerging powers, the G20, and reform of multilateral institutions’, 2024 (viewed on 23 April 2026) ↩

- 69 United Nations, ‘UN presents UN80 Initiative Action Plan, setting coordinated path for system-wide reforms’, November 2025 (viewed on 30 March 2026) ↩

- 70 MOPAN, ‘Multilateral Effectiveness in a Shifting Landscape: Mapping of Multilateral Organisations’ Response to the Current Funding Environment’, 2025, page 8 (viewed on 30 March 2026) ↩

- 71 Global Governance Institute, ‘Reforming the UN during a financial crisis: a foreseeable failure to align money, mandates, and majorities?’, July 2025 (viewed on 23 April 2026) ↩

- 72 International Monetary Fund Staff Discussion Note, ‘Geoeconomic fragmentation and the future of multilateralism’, 2023 (viewed on 23 April 2026) ↩

- 73 United Nations, UN Office for Digital and Emerging Technologies (viewed on 23 April 2026) ↩

- 74 Foreign Secretary statement on International Development: 19 March – GOV.UK (accessed 30/04/26). ↩